Last Saturday Warren Buffett’s 2012 letter to the shareholders of Berkshire Hathaway [PDF, 155 KB] was released. As always, I strongly encourage you to read it (23 pages).

From this year’s letter, I wanted to comment on 3 things:

- Lesson on dividends’ policy

- Books

- Running

****

Dividends’ Policy

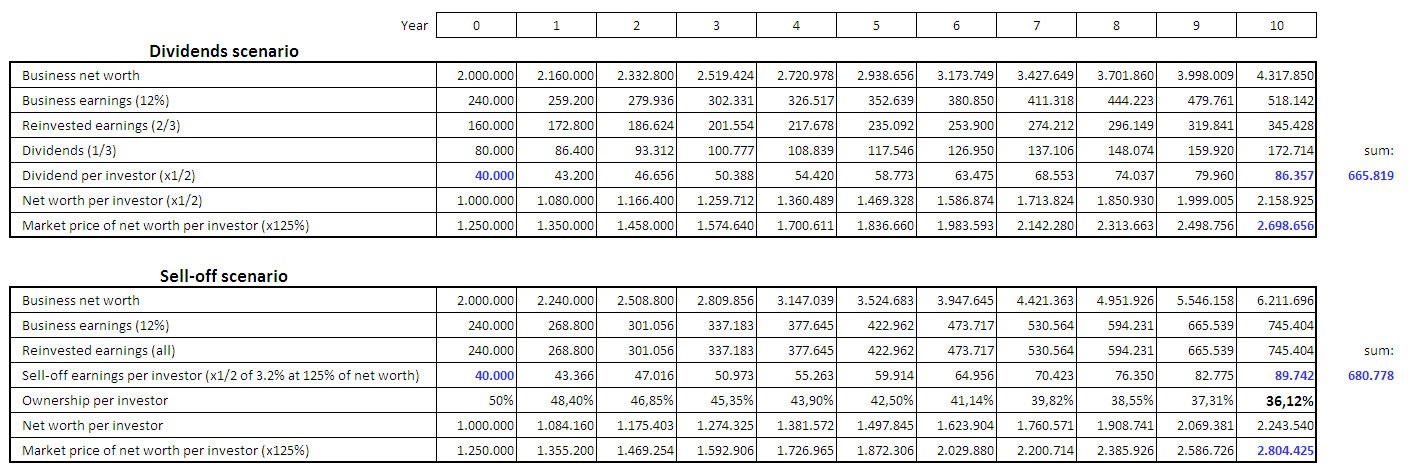

In my opinion the great lesson from this letter starts at page 18, when Warren explains the different ways a company has to allocate earnings. He makes a comparison between dividends and what he calls the “sell-off” scenario, where a shareholder can be better off when the company is not paying dividends and instead reinvesting all earnings while the shareholder sells part of his shares to obtain some cash.

See the explanation below (bit long):

“We’ll start by assuming that you and I are the equal owners of a business with $2 million of net worth. The business earns 12% on tangible net worth – $240,000 – and can reasonably expect to earn the same 12% on reinvested earnings. Furthermore, there are outsiders who always wish to buy into our business at 125% of net worth. Therefore, the value of what we each own is now $1.25 million.

You would like to have the two of us shareholders receive one-third of our company’s annual earnings and have two-thirds be reinvested. That plan, you feel, will nicely balance your needs for both current income and capital growth. So you suggest that we pay out $80,000 of current earnings and retain $160,000 to increase the future earnings of the business. In the first year, your dividend would be $40,000, and as earnings grew and the onethird payout was maintained, so too would your dividend. In total, dividends and stock value would increase 8% each year (12% earned on net worth less 4% of net worth paid out).

After ten years our company would have a net worth of $4,317,850 (the original $2 million compounded at 8%) and your dividend in the upcoming year would be $86,357. Each of us would have shares worth $2,698,656 (125% of our half of the company’s net worth). And we would live happily ever after – with dividends and the value of our stock continuing to grow at 8% annually.

There is an alternative approach, however, that would leave us even happier. Under this scenario, we would leave all earnings in the company and each sell 3.2% of our shares annually. Since the shares would be sold at 125% of book value, this approach would produce the same $40,000 of cash initially, a sum that would grow annually. Call this option the “sell-off” approach.

Under this “sell-off” scenario, the net worth of our company increases to $6,211,696 after ten years ($2 million compounded at 12%). Because we would be selling shares each year, our percentage ownership would have declined, and, after ten years, we would each own 36.12% of the business. Even so, your share of the net worth of the company at that time would be $2,243,540. And, remember, every dollar of net worth attributable to each of us can be sold for $1.25. Therefore, the market value of your remaining shares would be $2,804,425, about 4% greater than the value of your shares if we had followed the dividend approach.

Moreover, your annual cash receipts from the sell-off policy would now be running 4% more than you would have received under the dividend scenario. Voila! – you would have both more cash to spend annually and more capital value.”

As always, I believe that the best way is to make (play with) the numbers yourself, so you get to understand it once and for all. I paste here the numbers for those not being number-crunchers:

Buffett’s sell-off case vs. dividends.

Books

Over 2 years ago, I read Buffett’s biography “The Snowball: Warren Buffett and the Business of Life“, by Alice Schroeder (of which I wrote a post); it seems that I will have to get the newest one by Carol Loomis, “Tap Dancing to Work: Warren Buffett on Practically Everything“.

There is another book that I should read, according to the following passage in the letter:

“Above all, dividend policy should always be clear, consistent and rational. A capricious policy will confuse owners and drive away would-be investors. Phil Fisher put it wonderfully 54 years ago in Chapter 7 of his Common Stocks and Uncommon Profits, a book that ranks behind only The Intelligent Investor and the 1940 edition of Security Analysis in the all-time-best list for the serious investor. Phil explained that you can successfully run a restaurant that serves hamburgers or, alternatively, one that features Chinese food. But you can’t switch capriciously between the two and retain the fans of either.”

I’ve got all three books in the shelf since 5 years ago, it’s a shame that I have not yet read or gone through the first one!

Running

I found one final surprising and hilarious passage at the end of the letter embedded in the information related to the shareholders meeting:

“On Sunday at 8 a.m., we will initiate the “Berkshire 5K,” a race starting at the CenturyLink. Full details for participating will be included in the Visitor’s Guide that you will receive with your credentials for the meeting. We will have plenty of categories for competition, including one for the media. (It will be fun to report on their performance.) Regretfully, I will forego running; someone has to man the starting gun.

I should warn you that we have a lot of home-grown talent. Ted Weschler has run the marathon in 3:01. Jim Weber, Brooks’ dynamic CEO, is another speedster with a 3:31 best. Todd Combs specializes in the triathlon, but has been clocked at 22 minutes in the 5K.

That, however, is just the beginning: Our directors are also fleet of foot (that is, some of our directors are).Steve Burke has run an amazing 2:39 Boston marathon. (It’s a family thing; his wife, Gretchen, finished the New York marathon in 3:25.) Charlotte Guyman’s best is 3:37, and Sue Decker crossed the tape in New York in 3:36. Charlie did not return his questionnaire.”

I would have loved to take part in that race. I will probably do so in some other year :-).

Final confession

Luca and I went a couple of years ago to Berkshire Shareholder meeting. This year’s meeting will take place on May 4th.

This year, Luca and I will get married on May 11th, but one of the dates we considered was April 27th, and one of the drivers behind it was to be able to attend 2013 BRK meeting during the honeymoon…

Pingback: Transcript of 2014 Berkshire Hathaway Annual Q&A with Warren Buffett and Charlie Munger | The Blog by Javier

Pingback: Warren Buffett’s 2014 letter to the shareholders of Berkshire Hathaway | The Blog by Javier

Pingback: Warren Buffett’s 2015 letter to the shareholders of Berkshire Hathaway and 2016 annual shareholder meeting | The Blog by Javier

Pingback: Greg Abel’s 2025 letter to the shareholders of Berkshire Hathaway | The Blog by Javier