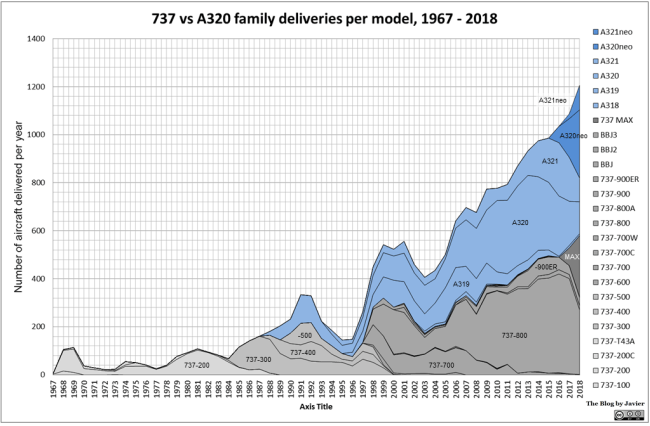

In the previous post I shared a graphic with the Boeing 737 deliveries per year per model since 1967 till 2018. In this post, I want to share a few graphics comparing the evolution of deliveries of the Boeing 737 family with the Airbus A320 family of aircraft.

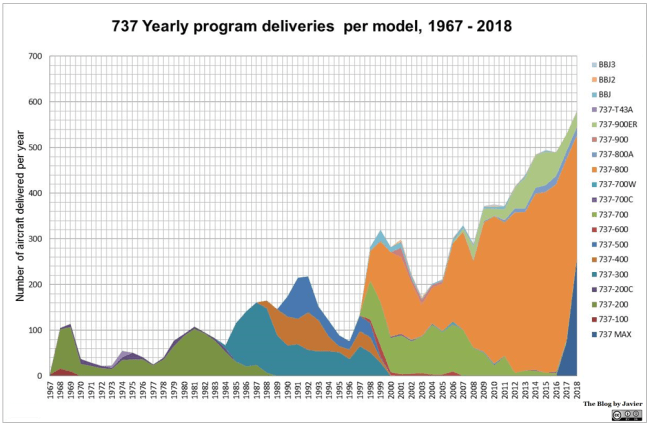

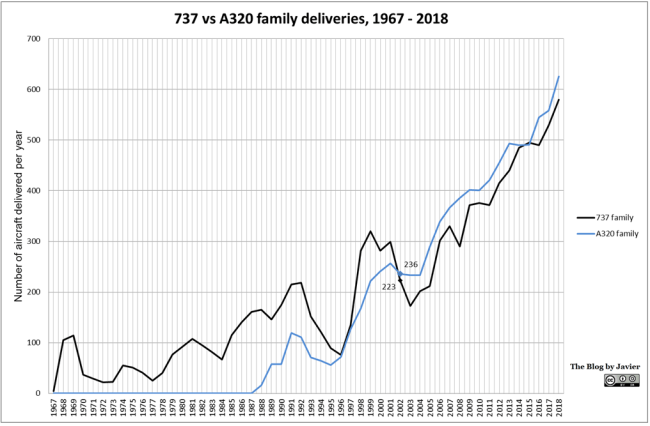

In the graphic you can see the tremendous growth in the past years. From the valley in 1995 (with 145 combined deliveries) till 2018 (with 1,206 combined deliveries) there has been a remarkable compound annual growth rate (CAGR) of 9.6%. The greatest sellers: the 737-800 with 4,959 aircraft delivered through end of 2018 and the A320 with 4,700.

The first time that the combined deliveries surpassed the 200 airplanes was in 1989 (204 aircraft). In 1998, the combined figure surpassed the 400 (450 aircraft). In 2012 they reached more than 800 (870). In 2016, more than 1,000 combined deliveries (1,035), reaching 1,206 in 2018.

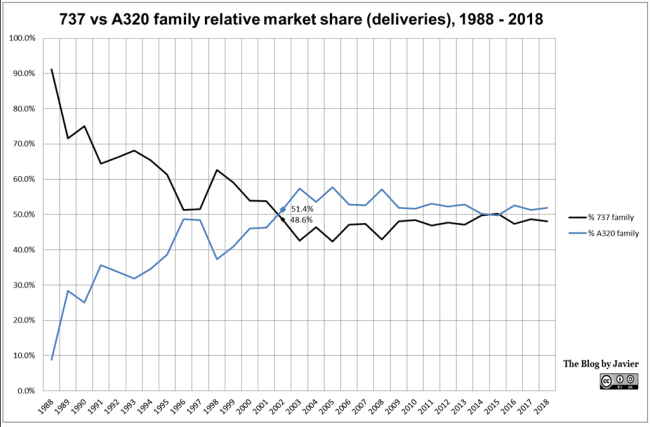

The A320 family surpassed the 737 family in yearly deliveries for the first time in the year 2002, when 236 aircraft of the family were delivered (85 A319, 116 A320 and 35 A321) compared to 223 737s. Since then Airbus has taken the lead in the relative market share between both families, with the exception of 2015 (49.8% – 50.2% for Boeing; with 4 aircraft making the difference – 491 vs 495).

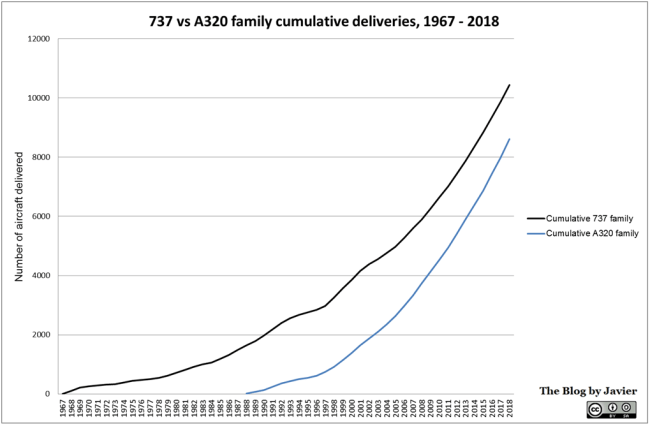

The 737 was introduced in 1967, the A320 in 1988, 21 years later. The 737 led the market for another 14 years, increasing the gap in aircraft deliveries. Since then Airbus has been narrowing it: at the end of 2018 the gap was of 1,839 aircraft with 10,444 cumulative 737s delivered compared to 8,605 A320s.