Two weeks ago, during Le Bourget air show in Paris, both Airbus and Boeing released their market forecasts for the following 20 years: Airbus’ Global Market Forecast (GMF, PDF 3.6 MB) and Boeing’s Current Market Outlook [PDF, 3.8 MB].

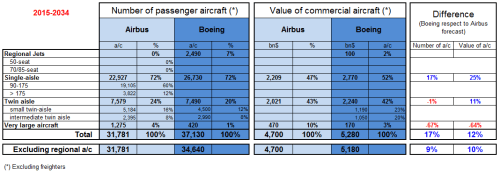

In previous years, I have published comparisons (1) of both Airbus’ and Boeing’s forecasts. You can find below the update of such comparison with the latest released figures from both companies.

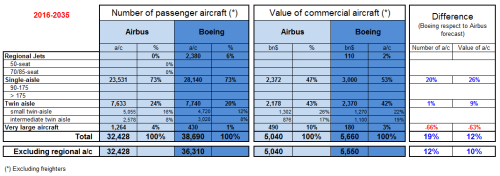

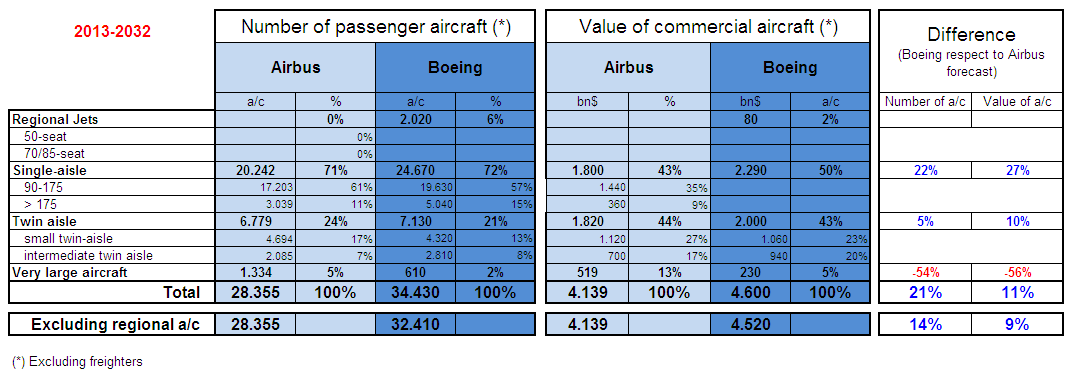

Comparison of Airbus GMF and Boeing CMO 2017-2036.

Some comments about the comparison:

- The main comment for this year CMO is that after years of Boeing dowplaying the demand for the segment of the large aircraft (seen as mainly 747, A380 and some other high capacity aircraft, depending on the manufacturer), it has finally stopped to consider them a category by themselves and has merged that category with the “intermediate twin-aisle” (i.e. 777, A350…).

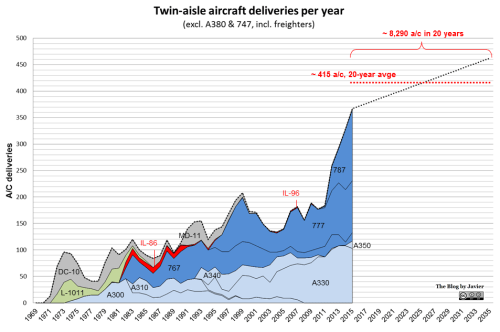

- Excluding the large aircraft, both companies’ forecast for the twin aisle segment is nearly identical: ~8,175-8,210 aircraft (we may assume that about 100 of those 8,210 from Boeing’s CMO correspond to large aircraft, thus comparing apple to apples would be ~8,175-8,100). The mix between small and intermediate twins varies, ~400 units up and down.

- On the other hand, Boeing forecasts about 4,700 single-aisle more than Airbus (the gap has widened in 100 units this year). Boeing doesn’t provide the split between more or less than 175 pax capacity airplanes since its 2015 CMO, nor does Airbus since 2016.

- Alltogether, Boeing sees demand for 10% more passenger aircraft (excluding regional a/c and freighters) with a 9% more value. The gap is slightly lower than in 2016.

- In relation to last year’s studies, Airbus has increased demand by ~1,700 aircraft (and ~ 190 Bn$) whereas Boeing has increased it by 1,400 (and ~ 130 Bn$).

- In relation to traffic, measured in terms of RPKs (“revenue passenger kilometer”), that is, the number of paying passenger by the distance they are transported, they see a similar future: Airbus forecasts for 2036 16.5 RPKs (in trillion, 4.4% annual growth from today) while Boeing forecasts 17.8 RPKs (4.7% annual growth).

Some lines to retain from this type of forecasts:

- Passenger world traffic (RPK) will continue to grow about 4.5% per year. This is, doubling every ~15 years.

- Today there are about 18,890 passenger aircraft around the world (according to Airbus; 19,130 in Boeing’s CMO), this number is about 800 a/c more than the year before (5% increase) and will more than double over the next 20 years to 40,120 a/c in 2036 (41,320 as seen by Boeing, excluding regional jets).

- Most deliveries will go to Asia-Pacific, 42% or ~17,000 passenger aircraft (according to Airbus).

- Domestic travel in China will be the largest traffic flow in 2036 with over 2,000 bn RPK (according to Boeing, an annual growth of 6.1%), or 11.6% of the World’s traffic.

- Nearly 13,000 aircraft will be retired to be replaced by more eco-efficient types.

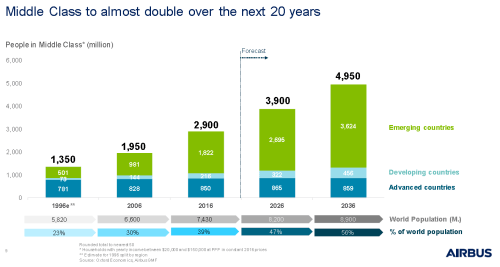

The doubling of the world’s middle class over the next 20 years will fuel air traffic growth and new airplanes demand.

As I do every year, I strongly recommend both documents (GMF and CMO) which provide a wealth of information of market dynamics.

(1) Find here the posts with similar comparisons I made with the forecasts of previous years: 2010, 2011, 2012, 2013, 2014, 2015, 2016.