Two weeks ago, on the second day of Farnborough air show, Boeing Commercial published its yearly update of the Current Market Outlook (CMO) for the next 20 years of commercial aircraft market (2018-2037).

I have just compared the figures for passenger aircraft of the last two years’ CMOs:

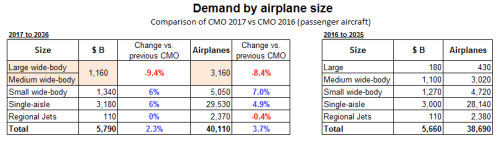

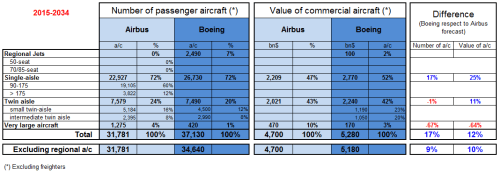

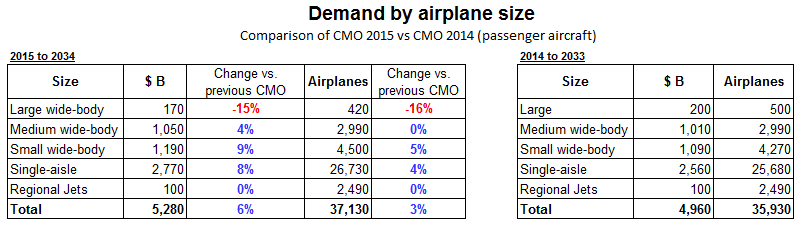

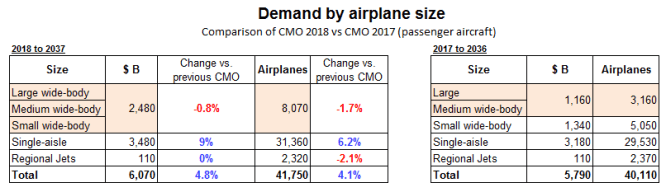

CMO 2018 vs. 2017 comparison.

Some comments to it:

- You can see that the total number of new aircraft delivered has slightly increased from 40,110 to 41,750, a 4.1%, which is consistent with the 4.7% traffic increase (1) that Boeing predicts (2).

- The volume (Bn$) increases by a higher percentage, 4.8% (280 Bn$) up to 6.07 Trn$. This is due to the increase in the single-aisle aircraft expected sales in volume (9%, +300 Bn$) and aircraft (6.2%, +1,830), as the other segments see both a forecast decrease in terms of volume and aircraft.

- For years, Boeing has been dowplaying in its CMO the demand for the segment of the large aircraft (seen as mainly 747, A380 and some other high capacity aircraft, depending on the manufacturer). Last year, Boeing stopped to consider them a category by themselves and merged that category with the “intermediate twin-aisle” (i.e. 777, A350…). This year, Boeing has further reduced the detail provided in the wide-body category by merging large aircraft with the small wide-body (i.e. 787, A330…) segments and now provides a single forecast for wide-body.

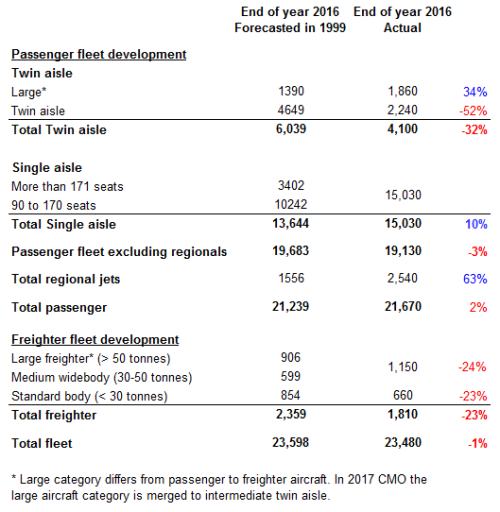

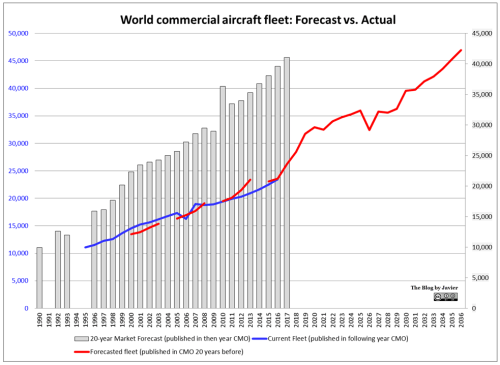

This year presentation did not include slides showing the accuracy of Boeing’s CMO of 20 years ago in predicting today’s fleet. They used to include such a slide in previous years’ presentations. I will come back to that in a following post.

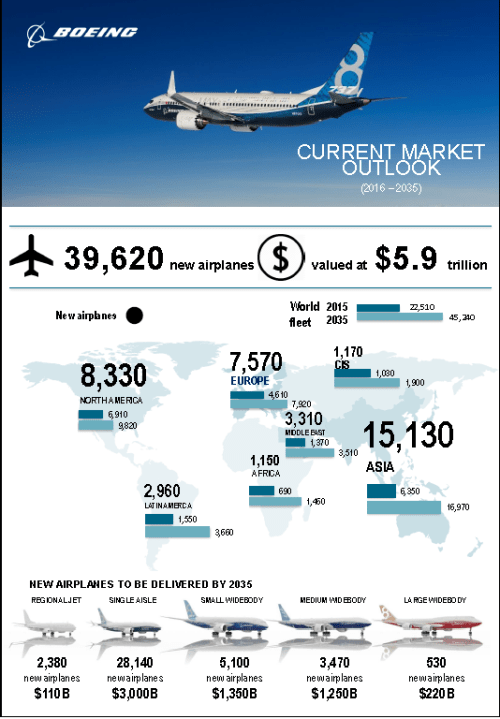

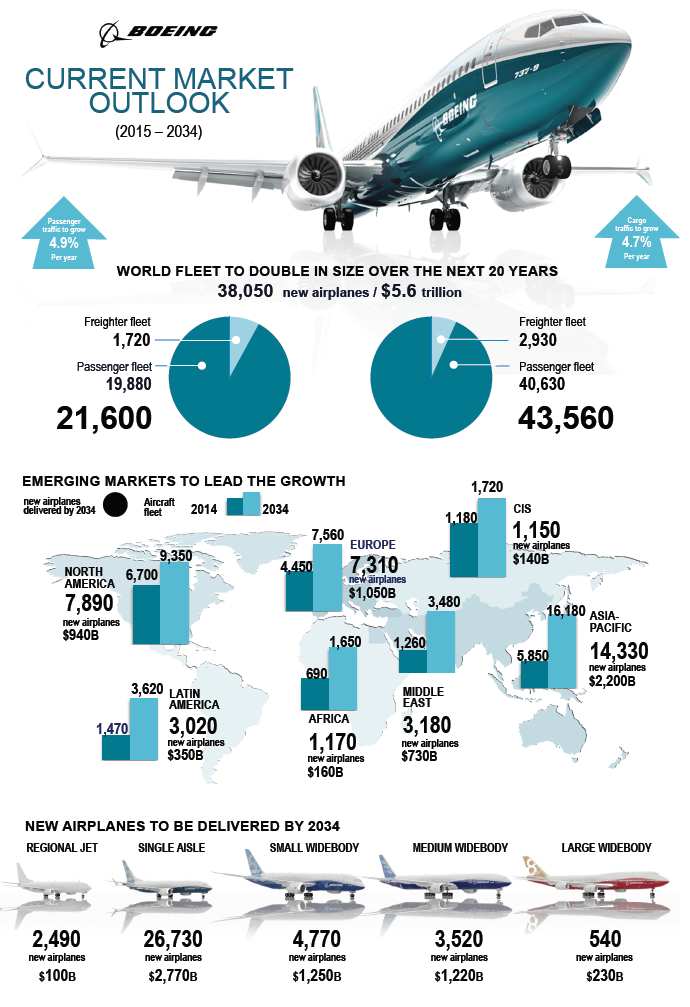

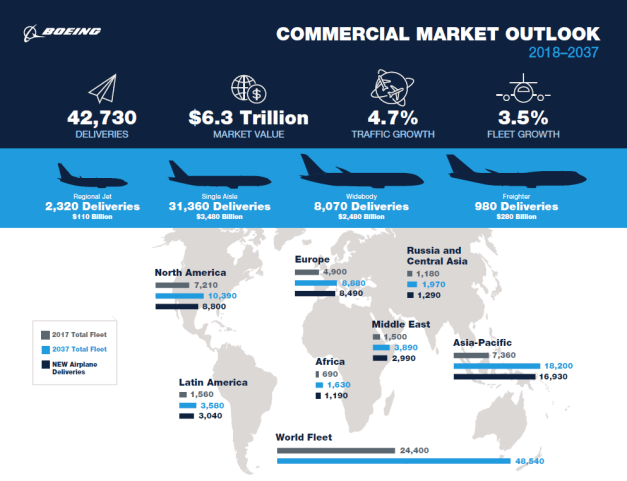

Find below a slide from the excutive summary [PDF, 263 kB] that provides a good snapshot of the forecast that the guys from Boeing have put up together:

As always, I recommend going through the CMO, as you can learn a lot about the business: from global numbers, to growth, traffic figures, fleet distributions, forecasts, etc… You may find the presentation [PDF, 5.1 MB], a file [XLS, 0.6 MB] with all the data or the full CMO report [PDF, 11 MB].

—

(1) Traffic increased measured in RPKS (revenue passenger kilometers) in trillions.

(2) These two ratios, 4.1% fleet demand and 4.7% traffic growth, point to an implicit increase in the average size of the aircraft in fleet and / or a higher utilization of the aircraft (higher availability).

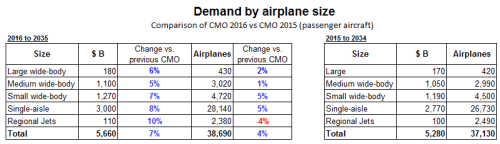

(3) Find the reviews I wrote comparing 2017 CMO with 2016 CMO, 2016 CMO with 2015 CMO, 2015 CMO with 2014 CMO, 2014 CMO with 2013 CMO and 2013 CMO with 2012 CMO.