Last Tuesday, John Leahy, Airbus COO Customers, unveiled at a press conference in London the new figures of the 2013-32 Airbus’ Global Market Forecast (GMF, PDF 5.1MB).

The last two years, I already published comparisons of both Airbus’ and Boeing’s forecasts (Current Market Outlook, CMO, PDF 3.0MB). You can find below the update of such comparison with the latest released figures from both companies.

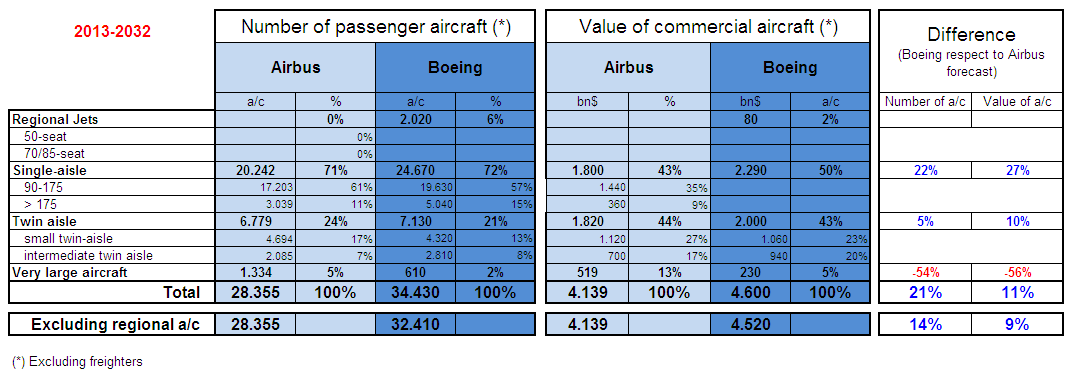

Comparison of Airbus GMF and Boeing CMO 2013-2032.

Some comments about the comparison:

- Boeing sees demand for 14% more passenger aircraft (excluding regional a/c, same proportion as last year) with a 9% more value (excluding freighters).

- Boeing continues to play down A380 niche potential (54% less a/c than Airbus’ GMF), though for third year in a row it has slightly increased its Very Large market forecast, again by 20 a/c, or 3.4%.

- On the other hand, Boeing forecasts about 350 twin-aisle and 4,400 single-aisle more than Airbus, clearly pointing to its point-to-point strategy versus the connecting mega-cities rationale presented by Airbus.

- In terms of RPKs (“revenue passenger kilometer”), that is, the number of paying passenger by the distance they are transported, they see a similar future: Airbus forecasts for 2032 ~14 RPKs (in trillion) (a ~9% increase vs last year GMF) while Boeing forecasts 14.7 (also increased about 7%).

The main changes from last year’s forecasts are:

- Both manufacturers have increased their passenger aircraft forecast, ~1,000 a/c Airbus and 1,400 a/c Boeing, bigger increase than last year’s change (500 a/c both).

- In the case of Airbus it has again mainly increased the single aisle segment (700 a/c), probably reflecting the success of the A320neo launch.

- In the case of Boeing, they decreased the twin aisle segment (80 a/c), but increased the single aisle in over 1,400 a/c.

- As I noted in a previous post, Boeing dramatically changed the twin-aisle mix, between small and intermediate. Now it has a mix closer to that of Airbus (60-70% of small twin-aisle).

- Both manufacturers have increased the value of RPKs in 2032 (9% and 7%).

- Both manufacturers have increased the volume (trn$) of the market in this 20 years, again 12% Airbus (to 4.1trn$) and 3% Boeing (to 4.5trn$) (excluding regionals and freighters).

Some catchy lines for those who have never seen these type of forecasts:

- Passenger world traffic (RPK) will continue to grow about 4.7% per year (5.0% according to Boeing). This is, doubling every ~15 years.

- Today there are about 16,100 passenger aircraft around the world (according to Airbus), this number will more than double in the next 20 years to above 33,600 a/c in 2032.

- 2/3 of the population of the emerging countries will take a trip a year in 2032.

- Domestic travel in China will be the largest traffic flow in 2032 with almost 1,400bn RPK, or 10% of the World’s traffic.

- The A20 family: a take-off every 2.5 seconds, with 99.6% reliability.

Trips per capita vs. GDP per capita (source: Airbus GMF).

As I do every year, I strongly recommend both documents (GMF and CMO) which provide a wealth of information of market dynamics. In case you find it tough, to read those kind of booklets, you may take a look at the video of the press conference, a great class on global economy, world aviation, forecasting, trend spotting (1h08’28”):