The Robin DR400 is a single engine piston aircraft very popular in France, with well over 2,000 units produced since its first version first flew back in the 1970s. That is the aircraft model I fly in the aeroclub and in this post I just wanted to share a few details about its construction, materials and a couple of pictures.

Pierre Robin founded the company Centre-Est Aéronautique in 1957 in Darois (France) together with the engineer Jean Délémontez at the time working for Jodel, from whom he took the wing dihedral. It is from their initials that comes the “DR”. Over the years the company first changed its name for Avions Pierre Robin, then it was sold… today the aircraft production is made together by Robin Aircraft and Centre-Est Aéronautique Pierre Robin (CEAPR).

In their website they explain the history of the DR400, first produced in 1972, and have a series of very interesting articles (in French) describing how they select and prepare the wood for their aircraft, how they build the wooden structure of the wings, how they build the wooden fuselage, how the wing skin is made out of a fabric produced by Diatex stapled to the frame (the craftsmen working on the fabric), the metallic parts of the plane… you read it well, a big share of the airframe is built out of wood and fabric, and this is to enable its light weight, between 615 and 630kg of manufacturer weight empty.

Recently, one of our aeroclub’s DR400s has gone through heavy maintenance, replacing the fabric and several parts and equipment. At the end of the process we received the pictures below of the wooden airframe:

Wing wooden structureFuselage wooden structure

Below you can see how the wing looks in flight, with the wooden structure covered by the fabric and how the lower pressure in the upper wing pulls up the fabric of the wing.

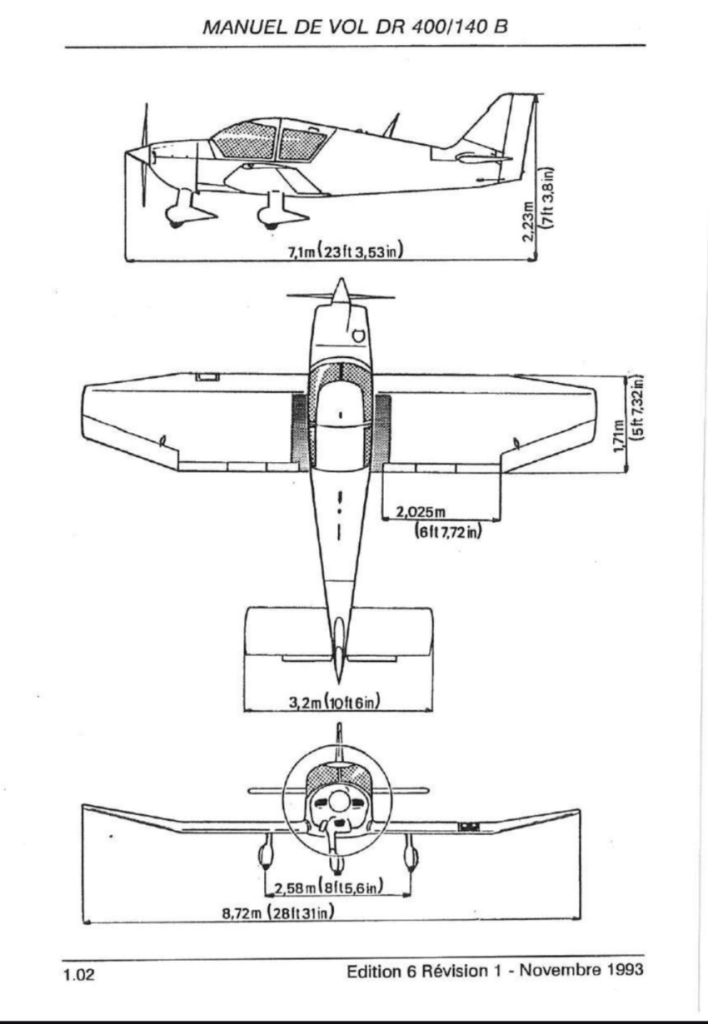

Wing in flightWing in flightDimensions of the DR400 as described in the Airplane Flight Manual

This post is to compare the compensation of Airbus and Boeing CEOs, with the recently published information of 2025 fiscal year, to have a record of the evolution (1) and for quick reference in different conversations.

As both Boeing and Airbus are public companies, the information about their CEOs compensation is public and can be found in the annual report and proxy statement from each one. I just share the information and sources below for comparison and future reference.

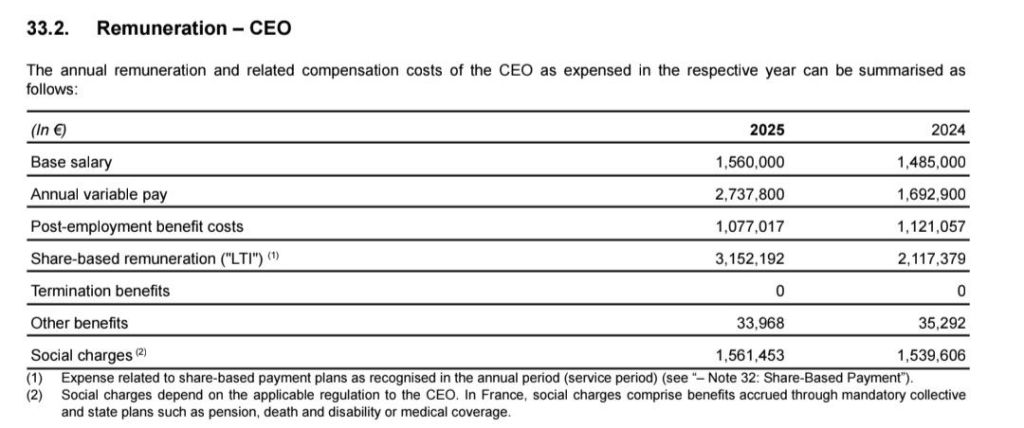

Faury had his base salary increased by 5% to 1.56M€ (which had been frozen in previous years and still at the level of 10 years ago). Variable pay increased by 62% to 2.74M€, post-employment benefit costs slightly decreased, share-based remuneration increased by 49% to 3.15M€ and social charges and other benefits slightly changed. Thus, the overall compensation at 10.12M€ increased 27% vs 2024 level (7.99M€) thanks mainly to the variable pay and share-based remuneration.

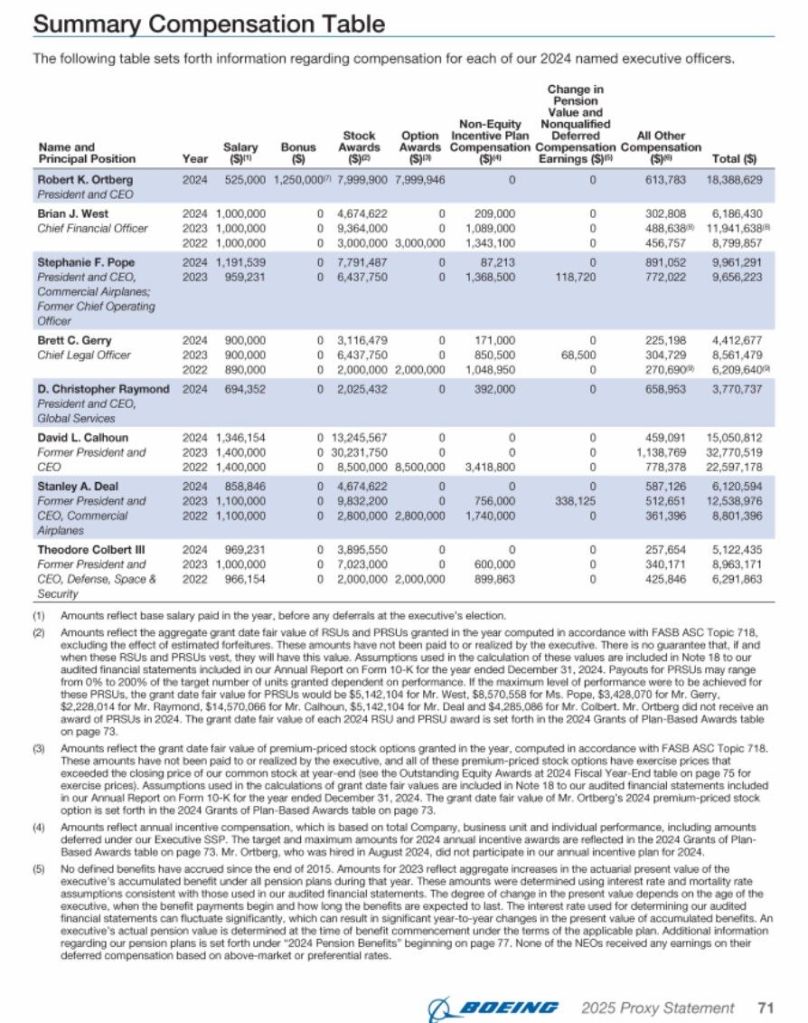

Boeing CEO, Robert Kelly Ortberg’s 2025 compensation (2026 proxy statement here, page 69):

Boeing’s CEO Robert Kelly Ortberg 2025 compensation.

Robert Kelly Ortberg had a base salary of 1.5M$ (up from 1.3M$ in 2023 for David Calhoun), received 17.5M$ in stocks and options based awards (9% up vs 2024), other 3.9M$ in non-equity incentive plan compensation and another 0.65M$ compensation item. The 2025 total compensation was 23.58M$, up from 2024 level but still below the 32.77M$ that Calhoun received in 2023.

Comparison. It is interesting to note that while the base salary is nearly the same in both companies, ~ 1.5 m€, the much higher stock based incentive schemes at Boeing pushed up the total remuneration for the CEO to about twice (x2.01) the one in Airbus.

For some years of the past decade (2013 to 2017), I wrote a small series of yearly posts comparing the compensation of Airbus and Boeing CEOs (1). This series started out of conversation with colleagues and I kept it updated to have a record of the evolution and for quick reference in other conversations. I then stopped the series. This post is just an update with the information for the 2024 fiscal year.

Many things happened in the industry in those 7 years (2017 to 2024), but if we focus just on the CEOs from both companies: Tom Enders was replaced by Guillaume Faury at the helm of Airbus; at Boeing, Dennis Muilenburg was replaced by David Calhoun who then left the place for Robert Kelly Ortberg.

As both Boeing and Airbus are public companies, the information about their CEOs compensation is public and can be found in the annual report and proxy statement from each one. I just share the information and sources below for comparison and future reference.

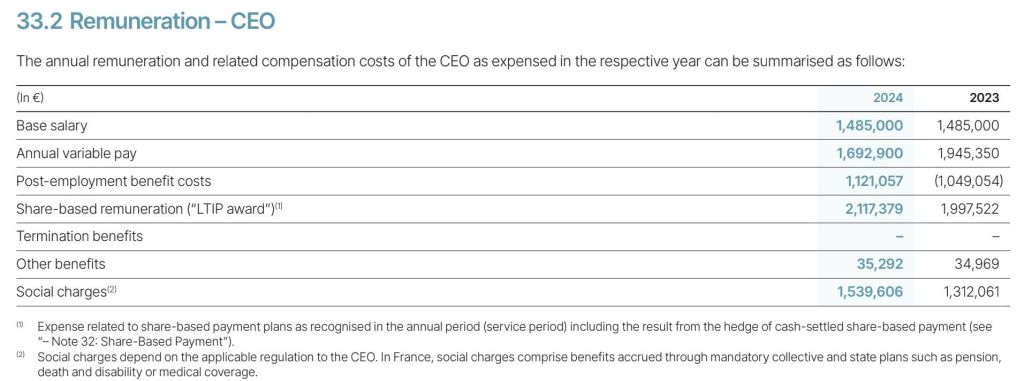

Faury had his base salary frozen in relation to 2024 at 1.485M€ (which is lower than Enders’ one at 1.5 M€ in 2017). Variable pay decreased in 13% to 1.69M€, post-employment benefit costs increased, as did share-based remuneration and social charges. In comparison to 2017, the main changes are the following two: 1) that there are no “Termination benefits” in 2024 while in 2017 Enders had announced his departure in 2019, thus the concept included 2.9M€, and 2) the exponential increase of social charges, 1.5M€ in 2024 vs 12k€ in 2017. Thus, the overall compensation at 7.99M€ increased vs 2023 but is below 2017 level (9.1 M€).

Boeing CEO, Robert Kelly Ortberg’s 2024 compensation (2025 proxy statement here, page 71):

Boeing’s CEO Robert Kelly Ortberg 2024 compensation.

Robert Kelly Ortberg had a base salary of 0.5M$, one bonus of 1.25M$ and 16M$ in stock based awards. The 2024 total compensation was 18.39M$, very similar to 2017 levels, but…

In the table you can also find the compensation for David Calhoun, and this is because Ortberg took over as CEO only in August of 2024. I will therefore add for comparison purposes the same table for Boeing 2023 fiscal year (2024 proxy here, page 72) when only Calhoun served as CEO.

Boeing’s CEO David Calhoun 2023 compensation.

David Calhoun had a base salary of 1.4M$, 30M$ in stock based awards and another 1.1M$ component. The 2023 total compensation was 32.77M$, 77% higher than 2017 levels, or +14M$.

Comparison. It is interesting to note that while the base salary is nearly the same in both companies, ~ 1.5 m€, the much higher stock based incentive schemes at Boeing push up the total remuneration for the CEO to about four times (x4.1) the one in Airbus.

A couple of months ago we visited for a second time the Luchtvaart Museum Aviodrome, the Aviation museum of The Netherlands, located in Lelystadt, a village on reclaimed land of the former Zuiderzee. The village was founded in 1967 and named after Cornelis Lely, the civil engineer behind the Afsluitdijk dyke. Shortly after, the construction of a local airport started and the first flights took place in 1971, in which today is the biggest general aviation airport in The Netherlands.

The museum is organized around 4 sections: the main indoor exhibition with a chronological tour through aviation history with a particular focus on Dutch contributions, the outdoors exhibition with a former KLM Boeing 747 open for visits as the main attraction, a hangar with some old aircraft with a Douglas DC-2 as main attraction and a replica of how Schiphol airport looked like in 1928.

Indoor exhibition

The main exhibition starts with the dawn of aviation from Da Vinci, to Montgolfier, to the Wright brothers, including some replicas and plenty of interactive games for kids to play with and understand some basics of aerodynamic, flight control, etc. Then the focus of the museum is on the Dutch side of aviation with the main characters of Anthony Fokker (aircraft designer), Frederick (Frits) Koolhoven (an automobile engineer turned aircraft designer) and KLM Royal Dutch Airlines with a focus on its first president Albert Plesman (who remained its CEO for 35 years until his death).

Some of the aircraft in the collection that I liked the most were the ones below:

Fokker Spin: Fokker’s first airplane.Fokker Dr.1: the famous triplane. The one flown by Manfred von Richthofen, the “Red Baron“, who created the aura with the nickname and red coloured plane to intimidate opponents in the air, who would immediately know they had such an effective ace on their tail!Spyker V.2: the first aircraft designed in the Netherlands to be produced in series.Fokker F.II: the first aircraft acquired by KLM with which KLM connected The Netherlands with England; also the first passenger airplane with a closed cabin.Fokker F.VII: which flew for the first time between The Netherlands and the Dutch East Indies, in 1924.Route from Amsterdam to Batavia (1933).Douglas DC-3: which KLM flew before WWII and until 1973.Douglas DC-3 fight deck.Lockheed L-749 Constellation.Lockheed L-749 Constellation flight deck.

Outdoors exhibition (747)

In the outdoors exhibition there are a few aircraft like a Fokker 100, a DC-4, an Antonov An-2, but the star is a former KLM Boeing 747 in combi configuration, where visitors can walk through the cargo deck, the economy and business classes and take a look into the flight deck. I leave some pictures below.

Boeing 747 from the upper deck.747 flight deck.747 business class cabin on the main deck.Cargo door in the rear fuselage.Rear pressure bulkhead.747 combi layout.Antonov An-2.Running loads written on the An-2 inner fuselage.

Hangar (DC-2)

The main item in the hangar is the DC-2 called “Uiver” that won the handicap competition of the MacRobertson Air Race (to commemorate Melbourne centenary celebrations) flying from London to Melbourne in 1934 (and came second in speed) covering 19,877km in 90 hours and 17 minutes. (The one in the exhibition is not the original Uiver as it crashed years after the race in operation; but another DC-2 restored and painted in the same colors)

DC-2 Uiver

Schiphol airport 1928 replica

I leave some pictures below of what was the hall with the counters of the different airlines, a schedule of KLM route to Batavia and some posters with references to the legendary ghost ship The Flying Dutchman.

The museum is great. For the international visitor it misses some panels’ translations. But you can easily follow most of it and spend as many hours as you please.

Yesterday, together with my family, we participated in a fly out excursion organized by Jean Claude and his aeroclub du Quercy for members of our Aviation Society. We came with different aircraft to meet at Cahors (LFCC) and from there, Jean Claude had prepared a closed loop circuit around the valleys of the rivers Lot and Dordogne, with several points to spot and some quizzes around the area.

Summary of the excursion

As our aeroclub is based in Toulouse Lasbordes (LFCL) we first had to fly to Cahors, a 40 minute flight.

Once at Cahors, we met different members of the local aeroclub and received a last briefing and some advice around the flight. The circuit was divided in 5 sectors.

Sector 1: in this sector we had to spot castles along the Lot, including the Château de Mercués (which belonged to Georges Héreil, former manager at Sud Aviation and father of the Caravelle), the Château de Caïx (acquired by Queen Marguerite II of Denmark, as her husband, prince Henrik, came from the region), Puy l’évêque and the Château de Bonaguil.

Sector 1Château de MercuésChâteau de Caïx

Sector 2: it consisted of flying North to reach the Dordogne, by way of Villefranche du Périgord.

Sector 3: in this sector we had to spot castles along the Dordogne, including the Château des Milandes (which belonged to the American French singer, activist, resistance agent Joséphine Baker – whose remains rest at the Pantheon), Beynac-et-Cazenac, La Roque, Domme, Souillac.

Sector 3Château des MilandesBeynac-et-CazenacLa Roque

Sector 4: in this sector we had to continue spotting castles along the Dordogne, including Château de la Treyne, Château de Belcastel and Château de Castelnau Bretenoux, we then turner South to fly over Saint Céré (home of the tapestry artist Jean Lurçat), then West towards the fall of Autoire (seemed dry from the air), Rocamadour and Labastide Murat (origin of the Marshal Joachim Murat).

Sector 4Château de la TreyneRocamadour

Sector 5: in this sector we went back to the valley of the Lot, by way of Marcilhac sur Célé, Cabrerets (where the Pech Merle cave is located, with its prehistoric cave paintings) and reaching Saint-Cirq-Lapopie. We then flew back to Cahors (birthplace of Leon Gambetta).

Sector 5Saint-Cirq-Lapopie

When we completed the circuit, we landed again at Cahors and shared a delicious lunch with the participants and members of the local aeroclub (very welcoming). They showed us as well the flight simulator they have developed in house to help with the training of new pilots.

Flight simulator at Cahors aeroclub du Quercy

Once, finished we bid our farewell and flew back to Toulouse.

I just realized mid February that Airbus market capitalization was higher than Boeing’s. At that point one was just above $125bn while the other was just below $123bn.

This is just a quick post to update those figures with today’s (March 11th, 2024) values at the closure of markets in NYSE and Paris, plus adding some historical perspective and evolution.

March 11th 2024

Airbus stock price: 156.8€, outstanding shares ~790.46 million (787.4 million at the end of 2023 as per the 2023 annual financial report), exchange rate 1.0926 $/€ … Airbus market capitalization ~ $135.4bn

Boeing stock price: 192.49$, outstanding shares ~610.1 million (610.1 million in January 2024 as per the 2023 annual financial report)… Boeing market capitalization ~ $117.4bn

Airbus market cap is 15% higher than Boeing’s

(This is not the first time that this happens. Looking back at the evolution of both stock prices and exchange rates, around mid May 2022 Airbus market cap was around 20% higher than Boeing’s.)

Now, looking back in time, at the end of 2012

Airbus stock price: 29.4€ (Dec 28th, last day of business), outstanding shares ~822.14 million (as per the 2012 annual financial report), exchange rate 1.3072 $/€ … Airbus market capitalization ~ $31.6bn

Boeing stock price: 75.36$ (Dec 31st, last day of business), outstanding shares ~755.6 million (as per the 2012 annual financial report)… Boeing market capitalization ~ $56.9bn

Boeing market cap was then 80% higher than Airbus’

Evolution from end 2012 to March 2024:

Airbus market cap has increased by x4.29 in these 11.19 years… share price increased by x5.33, hence yielding a compounded annual growth rate (CAGR) of 16.1%

Boeing market cap has increased by x2.06… share price increased by x2.55, yielding a 8.7% CAGR

As a final note, I leave here a link to an article from Leeham News and Analysis “Pontifications: A contrarian view of Stock Buybacks“, where they include a table with the cumulative investment by Boeing between 2013 and 2019 (both inclusive) in share buy backs, which amounts to $43.5bn.

Last weekend, with Luca and our children, we took one of the aeroclub’s DR-400 to make a flight excursion from Toulouse (France) to l’île d’Oléron, a small island close to La Rochelle.

North side of l’île d’Oléron

I had often heard about this destination from different members of our Aviation Society, so we wanted to give it a try as an easy plan for the weekend. We departed on Saturday morning from Toulouse Lasbordes (LFCL), flew to Saint Pierre d’Oléron (LFDP) in about 2h30′ and stayed overnight in the island, to come back the following morning.

In both flights we flew by the Dune of Pilat and Cap Ferret in order to enjoy the views of the coastline from that point all the way to l’île de Ré.

Cap Ferret

For the preparation of the flights and the navigation we relied on SkyDemon (I took again just 1 month subscription for 15€) from an iPad Mini (using an external GPS connected to the iPad). SkyDemon provides the GPS logs that afterwards can be viewed in Google Earth.

We did not reserve anything in advance, therefore upon arrival at the aerodrome we booked a couple of bikes at the aeroclub (20€ per bike per day; now I would suggest to book them in advance, as there were only 2 bikes left when we arrived) and a night at the hotell’Hermitage (very good breakfast, silent, nice warm swimming pool at the end of September and accepting payments with cheques vacances), close to the beach Sables Vignier Plage. We had packed light, just 3 light back packs, thus, we rode the bikes with the kids to the hotel and biked as well to and from the beach.

Biking to the hotel

Sables Vignier Plage

As an alternative airport I had selected La Rochelle, from which we could have taken a taxi to l’île de Ré. A third option would have been l’Île-d’Yeu which also has an aerodrome, but after a previous quick search in Booking.com I found that more hotel options with availability would be found at l’île d’Oléron. But I suggest to keep all options open, as if no hotels are found there, the other airports are at a short hop distance.

Saint Pierre d’Oléron (LFDP)

The kids preparing the airplane for the return flight

Two weeks ago, Jérémie and I took one of the aeroclub’s DR-400 airplanes (the 160hp F-GUYA) to make a flight excursion from Toulouse to the North Cape (Nordkapp, in Norway) as part of a “Fly out” organized by the Aviation Society of the Airbus Staff Council, together with 2 other aircraft, the F-BERB (with Norbert and Dominique, who organized the trip) and the F-PANI (with Anne and Nicolas).

At the beginning of the post I will focus on the different flights and share some pictures (taken either by me or Jérémie and Dominique, the ones with more quality) and at the bottom of the post I will leave some more technical details helpful for the preparation of such a trip.

We departed one day before the other airplanes to ensure that the engine hours of our airplane would not be consumed during a Saturday with good weather in Toulouse. However, North of Aurillac the weather was not so good so we waited until early in the afternoon to fly to Verdun. Even if not necessary we filed a flight plan and climbed to FL075 for most of the trip, to fly VFR on top of the clouds around the Massif Central and we just descended under the clouds some miles before the destination.

Once at Verdun we refueled the airplane, parked it for the night and booked a room at the Ibis budget hotel, which is however 5km from the aerodrome. A kind member of the local aeroclub gave us a lift to the hotel.

The morning after we did not have a transport to the aerodrome as apparently there were no taxis in the surroundings, so we had to walk to the airport; a hike that took us well over an hour with the bags and by some wheat fields.

We then made a short (~40′) flight to Doncourt, not without flying over some of the fields and memorial monuments of the WWI battle of Verdun. We then arrived to Doncourt, which has as A/A frenquency 123.500 and that was confusing as there are other aerodromes not too far using the same frequency, causing you to hear messages unrelated to the aerodrome you are about to land.

At Doncourt we refueled again and had a chat with a member of the local club. I went to pick some snacks from a local backery (less than 1km away) while we waited for the F-BERB. We then had a picnic at the aerodrome before departing for Tønder.

For the flight to Denmark we had to file a flight plan. We used a simple route based on the location of some VOR (DIK NOR BOT NDO). We were going to overfly Luxembourg and the whole of Germany. We climbed again to FL075 and were cleared (after the F-BERB) by the ATC (Langen radar) to fly through class C spaces around Cologne and Düsseldorf. Later, we listened in the radio that the F-BERB was descending to 3,000ft and below somewhere North of Bremen so we followed suit. From there and until nearly the border with Denmark the ceiling was at around 2,000ft, but since the ground is almost at sea level the flight was still comfortable. The West coastline of Schleswig-Holstein was wonderful.

Luxembourg, Essen, Duesseldorf

When we arrived at Tønder the F-PANI was already on ground and the F-BERB landed shortly after. Our flight plan had not been properly communicated and we were not expected, nor could refuel as we did not have local currency (DKK). We booked rooms in hotels in the village which was at walking distance. We then gathered at the Cafe Arthur and enjoyed our first dinner together as members of the fly out. There Dominique offered us a bottle of Saumur red wine that he had brought to celebrate that first night.

We woke up early as we wanted to be ready at the aerodrome at 7am to refuel the airplanes and had a 25-minute walk before to get to the aerodrome. The person in charge of the fuel station arrived a bit later but we were ready for departure at around 8am. We had filed another flight plan to fly to Bergen in Norway.

Flying over Denmark, despite its flatness, was nice, with the coast to the West, small crop fields and villages, including the coastal city of Esbjerg where my brother spent 2 weeks of the summer of 2002. We flew by the coast up until the village of Hanstholm (close to Thisted aerodrome) and then took a North West heading towards Norway with a transit of just above 30 minutes over the North Sea.

Once in Norway we continued flying along the Southern coast, overflying the airports of Farsund Lista, Stavanger Sola and Karmøy until we reached Bergen. During that flight of over 4 hours we enjoyed the good weather and the views.

At the tarmac in Bergen we spent some time between refueling and then waiting for the police to check our EU Covid-19 passport so that we were cleared to enter the country. We then purchased online the week pass covering the landing fees in all Norwegian airports, filed another flight plan and off we went for our next destination: Trondheim.

In that second flight, the sky was covered with clouds but the ceiling was not very low so it allowed for a relatively comfortable flight enjoying the views of the different islands. Once arrived at Trondheim we refueled, parked the plane, were taken in a small bus to the general aviation exit of the airport and walked to our hotel (Radisson Blu at the airport). We had dinner at the hotel restaurant and studied the weather which started to degrade.

Day 4 (July 20th) – Trondheim Værnes (ENVA) – Brønnøy (ENBN) – Bodø (ENBO) – Alta (ENAT)

In the first flight of the day we tried to reach Brønnøy overflying some fjords in the interior and flying over Namsos but before reaching that point there was no visibility and the F-PANI and us had to take a U-turn back to the fjord of Trondheim and get to the coastline overflying Orland airport. In flight we learnt that a NOTAM had been published informing that there was no Avgas that day at Brønnøy. Despite of that we landed there, which wasn’t easy as just when arriving there were some showers, so we had to hold first at the South and then changed our plan and approached the airport from the North West. At the airport we studied again the weather to the next airport where we could refuel, Bodø, a flight of just over an hour.

During the flight to Bodø we had a lower ceiling (at around 1,200ft, flying at below 1,000ft) and showers here and there. Though just at the airport the weather was clear. We landed, refueled, quickly ate some bananas and got ready for the next flight to Alta.

For the flight to Alta we would have liked to enjoy the view of the Lofoten islands, but seeing the weather and winds, we rather flew towards Leknes and then by the Western coastline of those islands. We passed by the West of Andenes. At that point the weather conditions were not very good, the flying was not easy. We counted with the help of the ATC and the messages exchanged between our 3 airplanes. Once we passed the latitude 70°, North of Tromsø, we got encouraging messages from the F-PANI, but as we were approaching Alta the weather was still not getting better, with very strong winds entering the Stjernsundet fjord to get to Alta. The airport in Alta was at the end of another fjord and at that point the wind was calmer and we landed.

The airport was closing so we just had time to get some help to get a taxi, book a room at the Scandic hotel and had dinner at Du Verden. The study of the weather during that dinner was not very positive, but we still gave us until the next morning to decide what to do the following day.

Day 5 (July 21st) – Alta

Before breakfast at 7am we looked at the weather and decided not to attempt to reach the North Cape that day, as the conditions were not very good with winds, rain and clouds. We booked another night at the hotel and the group split in two: Dominique and Norbert went to the airport to refuel the 3 planes, while the rest of us went to the museum of Alta to visit the Rock carvings (see related post). On the way there there was some rain but later on the sky became clear and we continued walking around for a total of more than 12km that day.

Back at the centre of the village we got some food for the plane (so we could have something to eat in the stops), we took a closer look at the iconic Northern Lights Cathedral and later met the group for dinner at a pizza restaurant, where again we studied the weather for the following morning, when we would attempt to fly by the North Cape followed by a flight to Tromsø.

Day 6 (July 22nd) – Alta (ENAT) – Alta (ENAT) – Bodø (ENBO)

We woke up early again, took breakfast together at 7am and got ready to go to the airport and wait for the weather to become more favorable. After about an hour, the F-BERB departed first by the fjord and then flying over the terrain to reach Porsangerfjord at the East and reach the North Cape from the South. A bit later the F-PANI and us left following the fjords (flying by Hammerfest) and reaching the North Cape from the West, took some pictures of it and then took heading for the South West.

The F-PANI flies much faster and at some point they reached a situation without visibility so they took a U-turn and so we did and both airplanes flew back to Alta, where we refueled again and stayed for some more time waiting for a front of clouds and rain to pass.

We then departed again, this time reaching the coast directly through the fjords to then follow the Western coast of the Lofoten islands on the way to Brønnøy. That flight was a very complex one. Already getting out of the fjords was difficult with very low ceiling, flying at 500ft, some showers, low visibility… flying with the help of the GPS to ascertain where the other side of the fjord or the next island would appear.

After 1h30′ the sky became somewhat clearer and just when we were going to fly West of Andenes airport we received a message from the F-BERB informing that the weather by the interior of the Lofoten islands was better and we could see some light from afar at that point so we changed plans and took heading for Evenes airport. We then enjoyed an hour of very pleasant flight over the islands and turquoise waters.

We flew past Bodø and exchanged some messages with the other airplanes about plans in Trondheim after refueling at Brønnøy only to find that some 40nm South of Bodø visibility was very bad and the ceiling very low. The difference now was that the area is full of small rocky islands, so at that point we made another U-turn and flew back to Bodø. The visibility at the airport was very low as well so we waited holding flying in circles at some 600ft for a few minutes about 20nm South of the airport until the controller offered to guide us to the airport under Special VFR.

We landed, refueled, called the tower by phone to thank the ATC for his help, booked a hotel by the harbor (Radisson Blu) and had dinner at Bjørk. Back at the hotel we studied the weather again and decided to go early to the airport to see if we could depart the following morning.

Day 7 (July 23rd) – Bodø

We reached the airport earlier than 7am to see if we could leave, but hesitated as the weather conditions were still quite degraded and were not getting better. After a couple of hours at the airport we gave up, called our colleagues at Trondheim (who then pursued their trip) and went back to book another hotel (Zefyr) and took the opportunity to visit the Norwegian Aviation Museum (see related post).

In the afternoon I went to rest at the hotel, while Jérémie went visiting around the city. For dinner we went to Burgasm (with a very comprehensive variety and customization of burgers).

Day 8 (July 24th) – Bodø

This day the weather was still pretty bad, as another low pressure front was coming from the South West and expected to hit the coast. We went to visit the Salmon centre by the harbor and then to the airport to move the airplane and align it with the strong winds that would blow later in the evening (and hopefully clear the local weather so that we could depart the following morning). That evening we had dinner at En Kopp, with very good fish dishes.

We left the hotel at 6am to try to be ready to fly at 7am and so we did. That day the weather was finally good, with just some clouds at 3,000ft around Bodø but clearing further South. We continued flying along the coast down to Brønnøy while climbing first to 4,500ft and then to 6,500ft in order to fly to the interior of the country, East of Trondheim, flying over Røros and approaching the TMA of Oslo Gardermoen from the North, flying by the East of the CTR and finally landing at Kjeller aerodrome (the first aerodrome built in Norway in 1912), where the weather was completely different, blue sky and hot temperatures.

Funnily enough, at the fuel station of Kjeller we met a local who had been in Toulouse learning to fly aerobatics and knew some members of one of the aeroclubs in Toulouse Lasbordes. We had lunch there, studied the weather again ahead of the crossing of the sea and the flight over Denmark, where storms were announced.

Shortly after we took off again from Kjeller, overflew Rygge and continued our flight to the South very close to the separation between the Norwegian and the Swedish FIR, while having the Swedish coast in sight for most of the time until we could see from afar the thin peninsula of Skagen in Denmark. This time we flew closer to the East of Jutland to avoid the storms that seemed to be more to the West. We left Aalborg to the West, then Billund and the ATC of Skrydstrup helped us in flying through some local cumulonimbus and showers, until we were finally in sight of Tønder.

At Tønder we met some of the members of the local club and later came the person in charge of the refueling station (as Norbert had called him to make sure they were aware of our arrival). This time we were able to pay in euros, so we refueled that same afternoon, before we were offered a lift to the Motel at the centre. We then went again to Cafe Arthur.

The following day would be a long one and the weather forecast wasn’t very good for Denmark or Luxembourg, but seemed OK to cross Germany. Following the example of the F-BERB we decided to go very early to the aerodrome to take off as soon as we could.

We woke up at 4:30am and left at 5:10 for the aerodrome. While walking the sky was clear, but when the aircraft was ready mist was taking over. When we were about to align on the runway we could not see further than half of it, so we went back to the parking, switched off the engine and waited a few minutes.

A bit later, when the mist seemed to have cleared a little bit and we had good visibility of the whole runway we tried again to take off and this time we went to the air leaving the low level mist below us and we continued our flight on top to the South, immediately crossing to Germany.

We flew at 4,500ft until Nordholz and then climbed to FL065 to have better visibility of the cities ahead of us. Later, ahead of reaching the class C spaces around Düsseldorf and Cologne the ATC gave us clearance and asked us to climb to FL070 to stay in VMC conditions, as around Cologne the clouds became more numerous and were quite abundant by the time we overflew Luxembourg.

Once we had crossed to the French air space we looked for a hole among the clouds so we could get below by flying down in circles making a downward spiral, and so we did, until we were below the ceiling at just around 1,000ft above ground level. We then informed the ATC of Strasbourg that we diverted to Doncourt instead of flying to Verdun, in order to land sooner instead of flying longer at that low altitude.

We then called the BRIA of Bordeaux to close the flight plan, refueled the plane, ate a little and studied the weather in France, which didn’t seem very good around the Massif Central nor West of it. After some careful study we guessed that the safest approach would be to make a small detour and fly South towards Toulouse by Dijon, Lyon, Nîmes, Montpellier and Carcassonne, and so we did.

We only encountered some showers before reaching Dijon, but further South the weather was good and we only had to watch out for some glider activity at some points around Lyon. We made a refueling stop at Alès Cévennes before getting ready for the last flight of the excursion.

Flying to Toulouse through the corridor of Montpellier – Carcassonne is something I had done a few times, so we just focused on staying alert as the day was getting long and we were becoming tired.

We finally landed at Toulouse Lasbordes, where Dominique and Norbert (who had arrived two days earlier) were waiting for us. They brought a bottle of champagne which we drank by the airplane still on the tarmac. They then helped us getting the airplane in the hangar, we said good-bye, continued cleaning the plane, filled in the papers… and savored the moment of what we had just accomplished: flying VFR all the way to the North Cape and back.

Trip preparation and tips

We flew for over 46 hours, the other plane departing from Toulouse did 43 hours. On flying days the average flying time was almost 7 hours per day, with a maximum over 9 hours the last day. We completed 15 flights.

We were stranded 3 days without flying, the other airplanes only 1, but the F-BERB in a similar excursion years ago also lost some 3 days. We also had to delay our departure by 4-5 days due to heavy rain in the North of France, Belgium and South of Germany around the targeted departure date. Thus, it would be prudent to budget in your calendar at least 10 days for the trip.

The excursion was mainly about flying, preparing flights, refueling, studying the weather (at dinners, breakfasts and refueling pauses). We only had time to visit the places when we were stranded. Thus, it is trip for dedicated aviation enthusiasts.

We opened an account at the Norwegian Avinor site. It’s free of charge and it contains all the aerodrome charts, AIP, weather information and a tool to file flight plans. In that site you’ll be able to get a week pass to cover all the landing fees for about 94€ (in July 2021).

For the preparation of the flights and the navigation we relied on SkyDemon (I took 1 month subscription for 14€) from an iPad Mini (however I used an external GPS connected to the iPad, this proved tricky for the battery management in the flights over 4 hours). The good resolution of SkyDemon was very valuable to fly along the coast when visibility was low.

Special attention needs to be paid to where you can refuel. About half of the airports in Norway do not have Avgas 100LL. Most of the ones that do have Avgas do not accept cash or credit card payment, but are divided into those which accept the Air BP card (which we had) and the ones accepting the Shell card (which we didn’t have, those part of the AFSN network – there was an AIP from just a few months before informing about that). Therefore we were effectively restricted to about one fourth of the airports (that is an element when thinking about flight planning and potential diversions, whether they may occur at the end or beginning of a flight). The best would be to depart with both the BP and the Shell cards.

All of the airports we landed were of moderate size with long runways.

The Norwegian ATC was quite helpful all along the trip and accommodated to many of our requests. When flying low sometimes we did not appear in their radar and sometimes the radio reception was poor, but those instances did not last long.

There was not much VFR traffic in the North, most of the other aircraft in the frequency were commercial aircraft from mostly Widerøe, Norwegian and SAS.

We did not make any hotel reservation in advance, only when landing at each airport in the afternoon, as we were not sure of whether we would be able to make it to the intended destination (a couple of times we didn’t). Once landed we made the reservations via booking.com.

The overall budget (including the cost of the flight hours including fuel (the largest cost by far), landing fees, hotels, meals, etc) for our plane has been around 9,500€ (less than 5,000€ per person).

During our flight excursion to Norway we had to stop for a couple of days in Bodø and this gave us the opportunity to visit the Norwegian Aviation Museum (Norsk luftfartsmuseum) built on the site of the airport built by the Germans during World War II.

The museum is divided mainly in two sections, military and civil aviation, which are separated by a hall which leads to a control tower that enjoys a good view over the airport of the city. We spent over 2 hours visiting the museum (entry price was 175 NOK, around 17 euros) and found it quite interesting.

Control Tower

Military aviation

The exhibition is organized chronologically, starting with the use of balloons to gather intelligence over the enemy lines in battles, the first pioneers in aviation and military aviation in between the world wars, the aircraft acquired for the armed forces in Norway at the time, the first military aerodrome in Norway (Kjeller) which was also the site where military aircraft would be produced under license, exhibits about operations during the second world war (such as the first paradropping operation over Stavanger Sola), the training of the Norwegian armed forces in Canada in a camp called “Little Norway“, and then ending with more modern aircraft.

Some of the relevant aircraft they have in display are: Avro 504K DYAK (used during WWI), Consolidated PBY-5A Catalina (amphibian aircraft mainly used for reconnaissance patrol of German U-boats), De Havilland DH.82 Tiger Moth (which was one of the aircraft licensed to be built at Kjeller between the wars and then was stationed at military bases in Kjeller, Værnes and Bardufoss), De Havilland DH 98 Mosquito (these were imported from Britain and several were lost during WWII missions mainly armed reconnaissance along the Norwegian coast and attacks on German U-boats), Supermarine Spitfire (the most important British fighter during WWII equipped as well two Norwegian squadrons which operated over 500 Spitfires between 1942 and 1945), etc.

Avro 504K

De Havilland DH 98 Mosquito

Supermarine Spitfire

Civil aviation

The civil aviation exhibition as well is organized chronologically, starting with the early pioneers who acquired some of the early models and studied aeronautical engineering in France, followed by the early development of aviation in Norway with emphasis on the role played by the former Norwegian Air Lines (DNL), Widerøe (regional airline connecting every corner of Norway and based in Bodø), Braathens and SAS.

The exhibition showcases as well some of the contributions of Norway to international aviation such as the development of navigational aids that enabled commercial traffic over polar regions (gyro compass, grid north and sky compass – read this interesting article on flying polar routes) thanks to the works of the navigator Einar Sverre Pedersen. The first polar route was operated by SAS in 1952 with a DC-6B, and then commercially from 1954 with Copenhagen to Los Angeles as the first route.

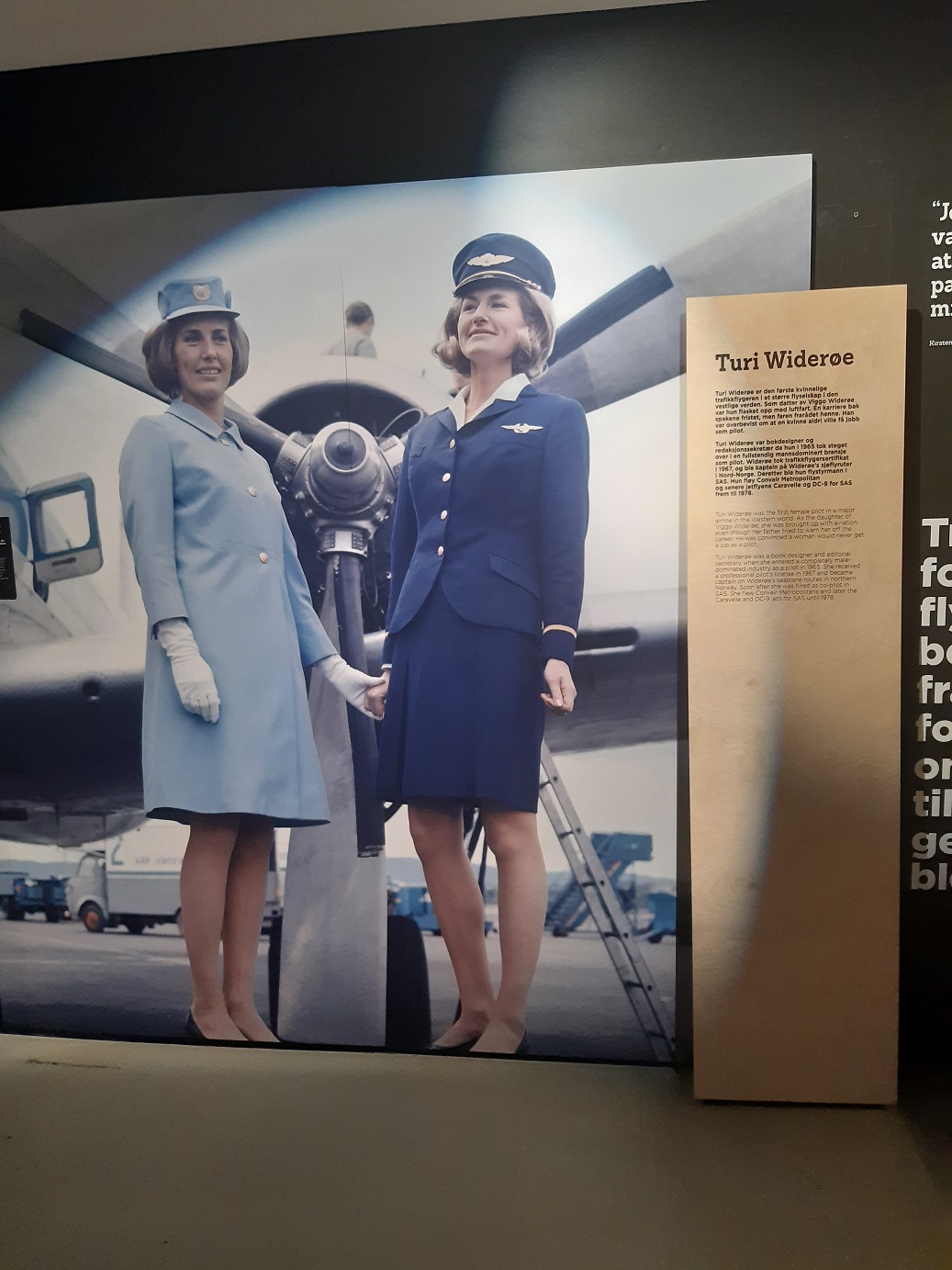

Another Norwegian breakthrough in commercial aviation consisted on Turi Widerøe (daughter of one of the founders of Widerøe airline) becoming the first female pilot in a major airline in the Western world in 1967, when she received her license; then she first operated seaplanes for Widerøe and later moved to SAS to fly Caravelles and DC-9s until her retirement in 1978.

This weekend, with my work colleague Thomas and other 7 airplanes of our Aviation Society, we made a day-long flight excursion to Biscarrosse (~60km South West of Bordeaux), in order to visit its Seaplane museum (Musée de l’Hydraviation).

We took the opportunity of the excursion to overfly other interesting landmarks such as the water slope of Montech, the pont-canal of Moissac, the Dune of Pilat and Cap Ferret by the bay of Arcachon.

I will be short in words in this post, thus I will first show here below some of the beautiful pictures of the flight (most taken by Thomas), and at the bottom I will include a few paragraphs with the technical information of the flight in case anyone is interested in planning a similar trip, and then I will briefly comment the museum.

Cap Ferret

Dune of Pilat

Dune of Pilat

Cap Ferret and Arcachon bay

Atlantic ocean

Lakes of Biscarrosse and Cazaux

Water slope at Montech

Aviation Society airplanes parked at Biscarrosse

Thomas and me

We made two flights. The first one from Toulouse Lasbordes (LFCL) to Biscarrosse Parentis (LFBS) lasted 2h05′ including the excursion to the seaside to overfly the Dune of Pilat and Cap Ferret, a detour of ~20′. The return trip took us 1h48′. Both trips could take somewhat less time if the routes were a bit more direct. We started both flights with the fuel tank full (in theory up to 109l of usable fuel) and after each flight we did refills of ~55 and 43 litres; that would mean a fuel consumption per trip of ~26.4l per hour and 23.9l per hour.

For the first flight we filed a flight plan (calling the BRIA of Bordeaux) even if not required in France (when not flying to the islands or abroad), but that eased the flying through different flight spaces, getting flight information service, traffic information, etc.

Flying around the Dune of Pilat and Arcachon bay was quite busy. We flew in the area at an altitude of ~2,500ft and below us, at around 1,000ft, we saw quite a few airplanes flying by, not all in the same radio frequency. Thus, in days of good weather that is something to watch out.

Biscarrosse-Parentis airport was also rather busy, with airplanes, ULMs, autogyros, helicopters and gliders… and seaplanes, some of them departing from the water but others from the paved runway, making use of small wheels installed in their floats. Luckily all the restricted airspace areas in the immediate surroundings of the airport were not active that day, otherwise it would have been trickier to approach the airport and be forced to fly at lower altitude.

The museum is at the other side of the village, not at walking distance. We were taken there by car by the director of the airport and his partner, thanks to their acquaintance with some of our society pilots; that helped a lot with the logistics, otherwise we would have taken taxis. There is a restaurant by the airport and another one by the museum, though we organized a picnic this time.

Musée de l’Hydraviation

At the beginning of the XX century Pierre-Georges Latécoère chose Biscarrosse to set up a seaplane assembly factory with parts coming from Toulouse. Latécoère seaplanes were among the largest French seaplanes produced (Latécoère 631) and from Biscarrosse Les Hourtiquets flying boat base departed air liners piloted by pioneers like Mermoz, Guillaumet or Saint-Exupery. Those were the days when Biscarrosse was destined to be one of the main hubs in aviation until the second world war came and aviation developed in a different path.

The museum takes less than 1h30′ to visit and it is mainly composed of models of the seaplanes of the early days (including the first attempts by Fabre and Curtis), the development and growth of Latécoère’s business, Boeing Clippers, the luxury of seaplane travel in those days, the role of seaplanes in the war, the dream that led to the single flight of the Hugues H-4 Hercules Spruce Goose, and today’s use of seaplanes in firefighting operations.

Grumman HU-16 Albatross

Fabre Hydravion model

Fabre Hydravion real scale model from recent years