Few days ago I gave my 100th micro credit with Kiva. This particular credit went to Philomene:

Philomene (image from Kiva).

“Philomene is 48 years old, married and has five children, ages 8 to 19. Her husband is a builder. She wants a loan to buy more fruits to sell, such as yellow bananas and passion fruit. The profits from savings will be used for paying children’s school fees.”

I got to know about Kiva from my friend Bruno at the end of 2008. I immediately liked the idea and I gave my first loan through it soon after, in January 2009.

The idea is very simple: giving micro credits via internet to small entrepreneurs in developing countries. Kiva facilitates the process establishing a website to channel the funds and creating network with local organizations which will disburse the money and collect repayments.

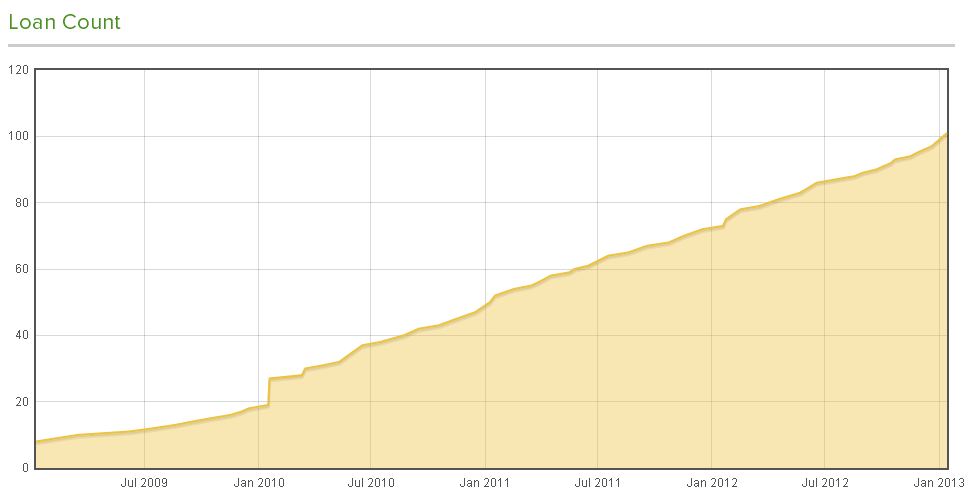

Since what you give is a credit, when it is paid back you can re-lend the money, thus, the same 25$ may be used by several entrepreneurs along the years. See my case:

Loan count since 2009.

The fact that I have given 101 credits of 25$, doesn’t mean I have dedicated 2,525$ in these 4 years. I have dedicated to Kiva just above 550$. With them I was able to lend and re-lend up to above 100 credits. Now I still have close to 400$ in outstanding credits (being re-paid), after having donated some 130$ to Kiva to help with their operating costs and having lost just 28.19$.

I want you to take a second to think what do those 28$ lost mean. The default rate along these 4 years in my case has been 1.5%, this is close to nothing. Take into account Western countries mortgage default rates: close to 10% in Spain, and though lower in USA it reached over 5% a few years back.

Of all the loans that should have already been paid (75) just 3 ended with a loss. In one I lost less than half of the 25$ and in other 2 thirds. The entrepreneurs came from Africa and I am not upset by not having gotten back 28$ from them. I just hope that their situation improved since the time they were forced to default. With the 3rd credit which ended in loss, I lost 0.06$… due to currency exchange, meaningless.

Do you want to know some more statistics?

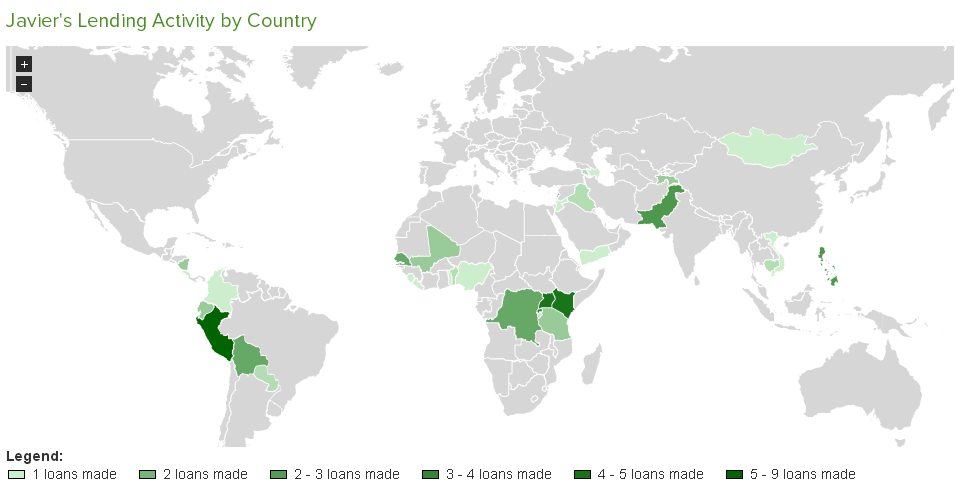

See below a map with coloured countries being the ones in which a recipient of one of my credit lives:

My “Lending by Country” map.

- In 67% of the cases the recipient of my loans are women (see Forbes article about higher ROI when investing in women).

- The countries in which I have given more credits: Peru (see the story about one of the entrepreneurs there that I visited), Uganda, Kenya, Rwanda, Philippines, Pakistan…

- Regarding sectors: agriculture takes 30.7% of my credits, followed by food (22.8%), manufacturing (13.9%), retail (10.9%), education (6.9%)… (I would like to give more credits for education, but within Kiva there are not so many displayed; to cover that need I collaborate with another organization, Vittana).

- I told you that I was introduced to Kiva by a friend. I also sent many invitations and some gift cards to friends; 6 of my friends accepted them.

These were my first 101 loans. Loans that change lives…