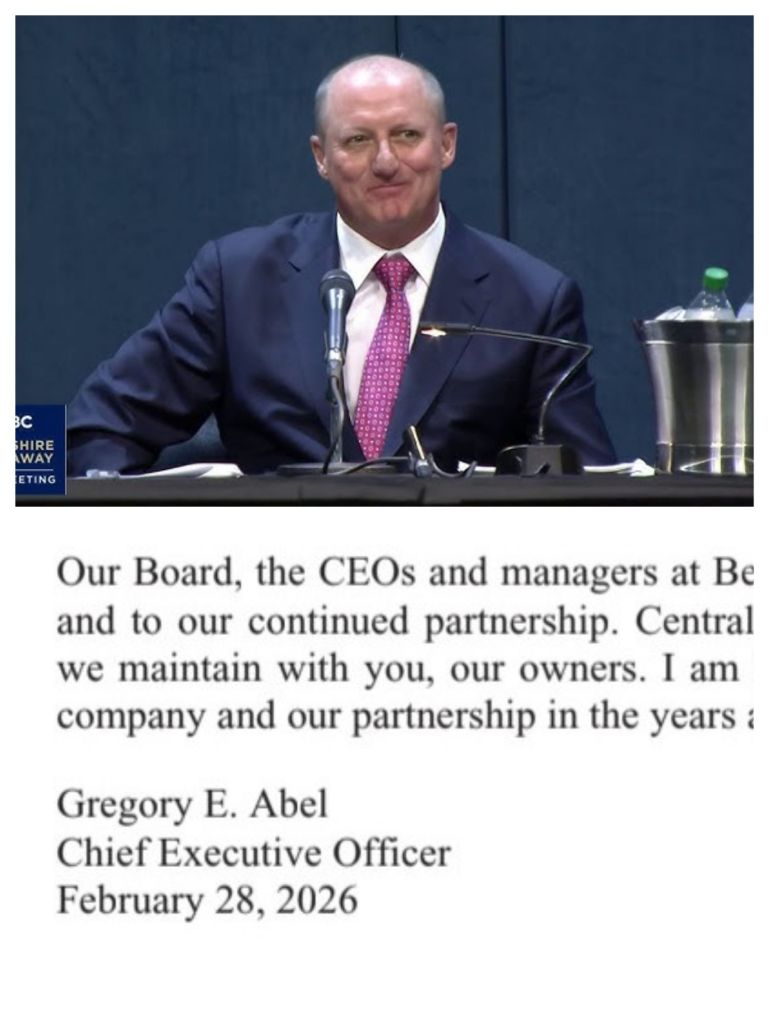

Every last Saturday of February, a must read for the weekend comes out: the letter to the Shareholders of Berkshire Hathaway by its CEO. For decades this was Warren Buffett’s letter, today it was the first such letter by Greg Abel [PDF, 91kB], the new CEO of the company, after Buffett stepped aside, remaining as chairman of the board.

To publish Abel’s letters they have created a new section in the rather rustic website of the conglomerate:

The new CEO chose the following words to open his first letter to the shareholders:

To My Fellow Berkshire Shareholders,

He then dedicated some lines of tribute to his predecessor and later to Charlie Munger.

The overarching theme of this year’s letter was to emphasize the culture and values of Berkshire, which he is fully committed to preserve, as he reflected by sharing this past comment:

Charlie’s comment on May 1, 2021, that “Greg will keep the culture” will forever resonate with me. It was a reminder that our culture is our most treasured asset, a call to maintain what defines Berkshire, and a challenge to ensure our culture continues.

Before discussing the performance of the different businesses in 2025 he chose to share a letter he sent earlier this year to the employees, which he commented by adding further context and details at some points.

I share below some excerpts that called my attention.

On integrity, recalling the past:

… we played a clip from Warren’s 1991 Salomon Brothers Congressional testimony: “Lose money for the firm, and I will be understanding; lose a shred of reputation for the firm, and I will be ruthless.”

We know integrity is not a quality you admire on a shelf; it is an active quality that must be earned, re-earned, and maintained daily.

On the group’s financial strength:

… financial strength by using debt sparingly and prudently.

On the line between being a responsible company (integrity) accountable for its actions and defending its shareholders;

Where responsibility does not exist, it will continue to seek judicial relief. Accountability, paired with principled opposition to unwarranted liability, is essential to preserving the regulatory compact that governs utilities.

On its main equity investments, four American companies (Apple, American Express, Coca-Cola, and Moody’s; combined market value of these investments $158.6bn) and five Japanese ones ($35bn):

Taking these positions together, at year-end they totaled $194 billion in market value, representing nearly two-thirds of our $297.8 billion equity securities portfolio, providing combined dividends of $2.5 billion and yielding 10% on their original cost basis of $24.5 billion.

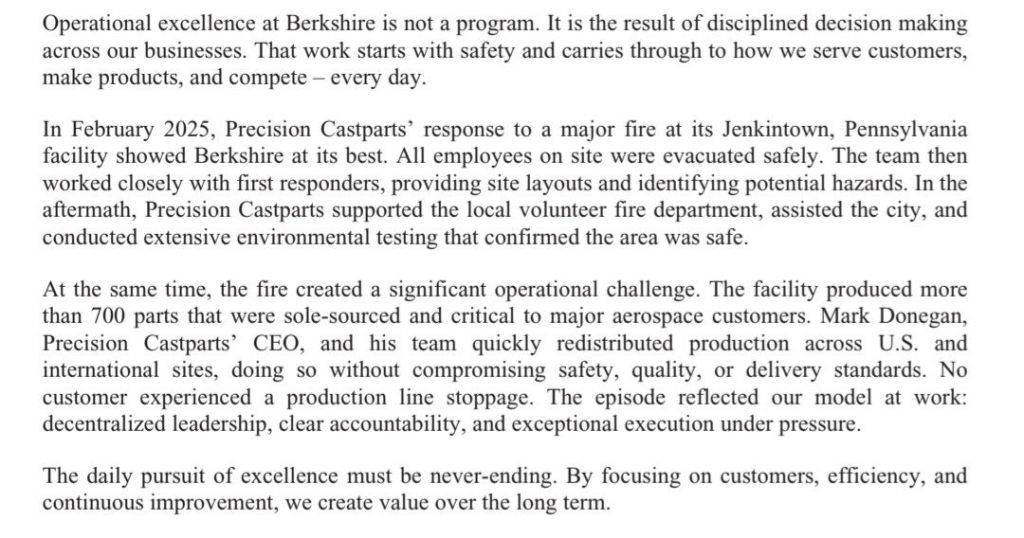

I also like the explanation of how the fire at Precision Castparts was handled, when discussing operational excellence:

Finally, he closed the letter by sharing some details about the annual shareholders meeting next May 2nd, where he confirmed he will be on stage to answer questions from the audience. The exercise will be a more choral one, compared to the old days of Warren Buffett and Charlie Munger, though in the last years Greg Abel and Ajit Jain already joined Buffett on stage.

This year’s program will include a CEO’s update on Berkshire, and two Q&A sessions – one with Ajit and me, and a second featuring Katie Farmer (BNSF), Adam Johnson (NetJets and president of consumer products, service, and retailing), and me, where Katie and Adam will discuss the challenges and opportunities they see in their respective businesses.

A new era at Berkshire Hathaway is starting.

(1) See the review I made of 2009, 2012, 2013, 2014 and 2015 letters.

(2) See here the review I made of the 2011 annual shareholder’s meeting when we attended it in Omaha.