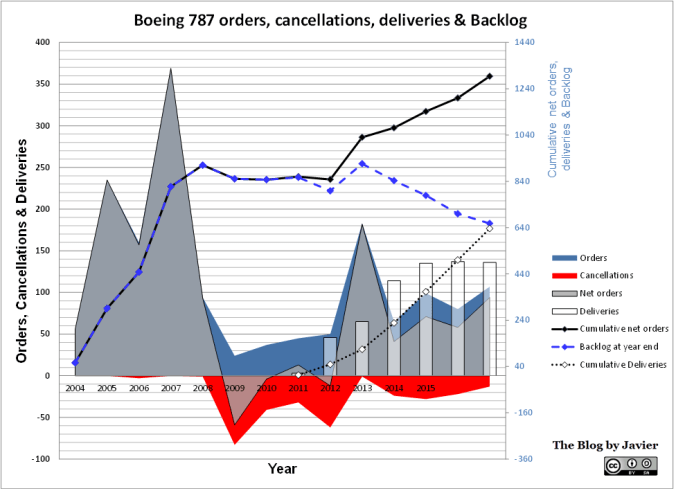

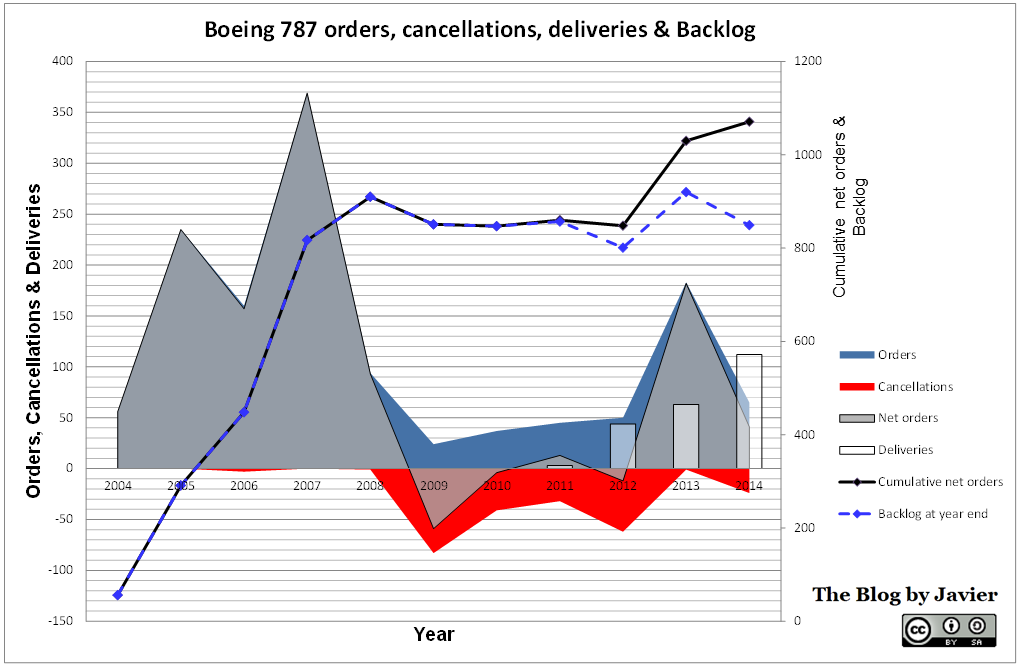

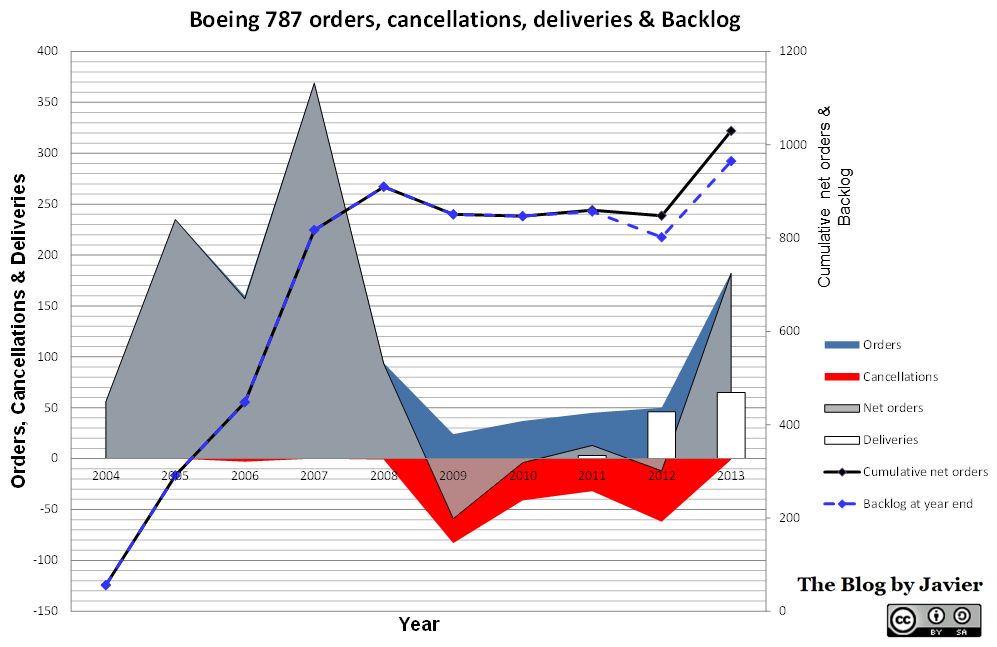

Some weeks ago, Boeing released 2011 results [PDF, 252KB]. The company reported revenues of almost 69bn$, 477 commercial deliveries and 805 net orders for its commercial aircraft. All these were widely reported by the media and mean a good year for Boeing.

Last years I wrote in some posts what was my estimate of Boeing discounts: the relation between what is announced by the press, what appears in its list prices and sometimes as backlogs and what it is indeed computed into the profit and loss account. In this post I wanted to update, if necessary, the figure I calculated for the average discount of Boeing.

Most of the necessary information can be found in its website. Boeing list prices can be found here.

The number of gross and net orders (after cancellations) year by year can be found here.

Last year deliveries can be found in the report of financial results. From there we can also deduct the figure of Boeing Commercial’s sales of services. That is not directly reported but can be deducted (all Boeing services-related sales are reported as well as Boeing Capital Corporation division and Boeing Defense’s “Global Services & Support” unit)

As in the post of last year:

- I needed to make one assumption: new orders come with a 3% down payment in the year of the booking, while the remaining cost I assumed that was paid on the year of delivery (for simplicity I didn’t consider more intermediate revenue recognition milestones linked to payments, the 3% figure was taken from the AIAA paper “A Hierarchical Aircraft Life Cycle Cost Analysis Model” by William J. Marx et al.). [1]

Having put all the figures together, the calculation is immediate. Boeing Commercial Aircraft revenues in 2011 (36,2bn$) are the sum of:

- the discounted prices times the delivered aircraft in the year (including possible penalties from delays),

- less the down payment of the current year delivered aircraft, as the down payment was included in previous years results,

- plus the down payment of current year net orders (this year’s this calculation was a bit trickier as it included 737NG deliveries BUT 737 MAX orders),

- plus services revenues.

The discount figure that minimized errors last year was 41%. Using this figure, the error obtained this year in relation to Boeing Commercial Aircraft reported revenues is 0.1%. That is a little higher discount than previous years (39% for 2010 and 38% for 2009). The only explanation for that would be the built-in penalties for 787 and 747 delays into revenues plus the launch of a new aircraft, 737 MAX.

Thus, the updated discount for Boeing commercial aircraft is 41% (!).

—

[1] Last year, I received a comment from the analyst Scott Hamilton on the level of downpayments. He mentioned they could reach up to 30%. I tried this time to compute the calculation using that input, but the figures of discounts to be applied each year to minimize errors are not consistent, thus I stayed with the 3% used in the above-mentioned published paper.