Shuffling books among shelfs at home a few days ago, I came across “Confusión de Confusiones” by José de la Vega (“Confusion of Confusions“ in English). This is a book I had referred to a couple of times in this blog but I never wrote about it.

José de la Vega was born in the province of Córdoba in Spain in around 1650. The family, Jewish, moved to today’s Netherlands to profess its faith. In 1688, he wrote Confusión de Confusiones, the oldest book ever written about the stock exchange business. The book takes the form of a dialogue between a shareholder, a philosopher and a businessman.

I read a hard cover Spanish version of the book edited by Macanaz. The editors did a great job. The book includes a ~30-pages dictionary at the end translating old Spanish words, Latin words, providing explanations for characters and places mentioned, etc. It also includes a 5-pages recap of the main advises José de la Vega provides to investors along the book.

The Amsterdam stock market at that time suffered from all the ailments that stock markets suffer today: hysteria, bulls and bears, irrationality, information asymmetry, etc. It is worth noting that the stock market at that time consisted of: one single trading place, Amsterdam, and one single company, the Dutch East India Company (Vereenigde Oost-Indische Compagnie, VOC). This may lead to think that everything should be quieter at that time, but as the author notes (1):

[…] you shall know that the Shares have three stimuli to go up and another three to go down: the status of India, the disposition of Europe and the gambling of the Shareholders. Thus, very often the news do not produce any benefit, because they take the flows to another direction.

The health of the business, the mood in the market place and the selling and buying of investors and speculators. That is all that it takes to provoke the financial ups and downs that in the end cause stock market crashes.

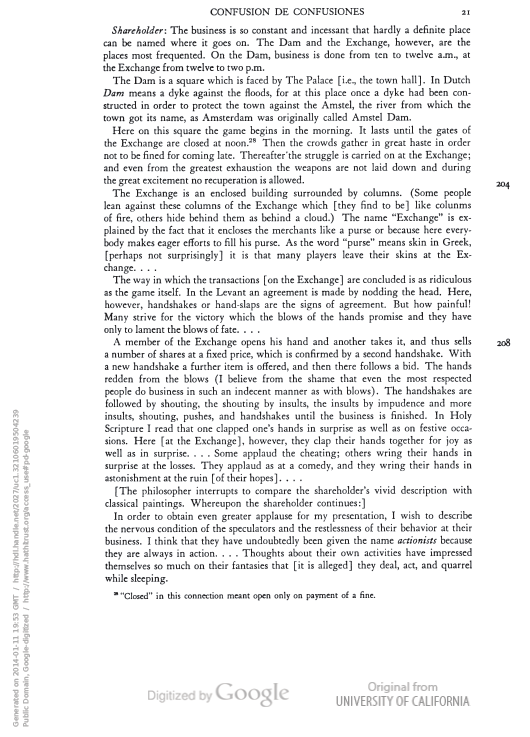

About the place and the way the market operated, he explained (extract from Google digitized English version, public domain, which however omits some paragraphs):

Extract from “Confusión de Confusiones”.

To conclude with the comments on the book I will include here some of the advises from the author, first in Spanish so the readers of the blog who understand it can capture the language and then translated:

“Los necios, que de todo se afligen, de todo se lamentan, de todo se desesperan.”

“Los que están con la soga en la garganta no tienen otro cortejo que de verdugos.”

“¿Qué vale no arriesgar la hacienda, si se pierde el Alma?”

“Si el que compra algunas partidas, ve que bajan, rabia de haber comprado, si suben, rabia de que no compró más; si compra, suben, vende, gana, y vuelan aun a más alto precio del que ha vendido, rabia de que vendió por menor precio; si no compra ni vende, y van subiendo, rabia de que habiendo tenido impulsos de comprar, no llegó a lograr los impulsos.”

“En acciones no se debe dar consejo a nadie, porque donde está encantado el acierto, mal puede lucir airoso el consejo.”

“La máxima de los accionistas veteranos, es No casarse con las Acciones.”

“En perdiendo esperar, en ganando recoger.”

“Es ignorancia haberos dejado engañar, porque precediendo para la constancia tantos avisos, no pueden tener descargo los errores.”

“No quieren apercibir esta filosofía los inquietos, y como son aire, y es aire lo que tratan, para fabricar torres en el aire, juzgan que cuanto más se mueven más se exaltan, cuanto más se agitan más se calientan, y cuanto más se calientan más crecen.”

“Quien tal hace, que tal pague.”

“El punto no estaba en ver cómo se había de entrar, sino en considerar cómo se había de salir.”

… (see translations below (2))

Each of those sentences would suggest a topic for a whole post in itself; advisors, frequent trading, bubbles, short-term view, banks bail outs, etc…

The book is great, however it is quite difficult to read. Jose de la Vega lived in 1688 and was a philosopher; be prepared for the language he uses and the use of ancient History episodes to illustrate his explanations.

Finally, researching for this post I learned in the Wikipedia that the Federation of European Securities Exchanges (FESE) awards each year a prize honouring De la Vega to authors of outstanding research related to the securities markets in Europe. You can see here the list of winners of the prize.

Curiously enough, the 2013 prize went to Sophie Moinas from Toulouse School of Economics, for her paper “Liquidity Supply across Multiple Trading Venues” (jointly with Laurence Lescourret).

—

(1) Translations are mine, as I noted the book I have is a Spanish version of it.

(2) Translations of the advises:

“Fools, they grieve about everything, lament everything, despair with everything.”

“The ones with the rope in the throat are not courted by anyone but executioners.”

“What is it worth not to bet the house, if the soul is lost?”

“The one who buy some shares, if they, is angry at having bought, if they go up , is angry because he did not buy more; if he buys, they go up, sells, wins, and the share fly even higher than the price at which he sold, he is angry for having sold at a lower price; if he neither bought nor sold, and he sees the shares going up, he is angry because having had buying impulses, he failed to buy.”

“Regarding shares one should not give advice to anyone, because where success is haunted, it is difficult that the advice looks graceful.”

“The mantra of veteran shareholders, is Not marry the Shares.”

“When losing wait, when winning collect.”

“You have been an ignorant for having let yourself fooled, because preceding such a record of warnings, there can not be excuse for errors. “

“The restless do not want to embrace this philosophy, and like the air they are, and air is what they trade, to build castles in the air, they judge that the more they move the more exalted they are, the more agitated they are more over heated they become, and the more hotter they become they grow more.”

“He who does that, he who shall pay that.”

“The point was not in seeing how to enter in it, but in considering how to exit.”