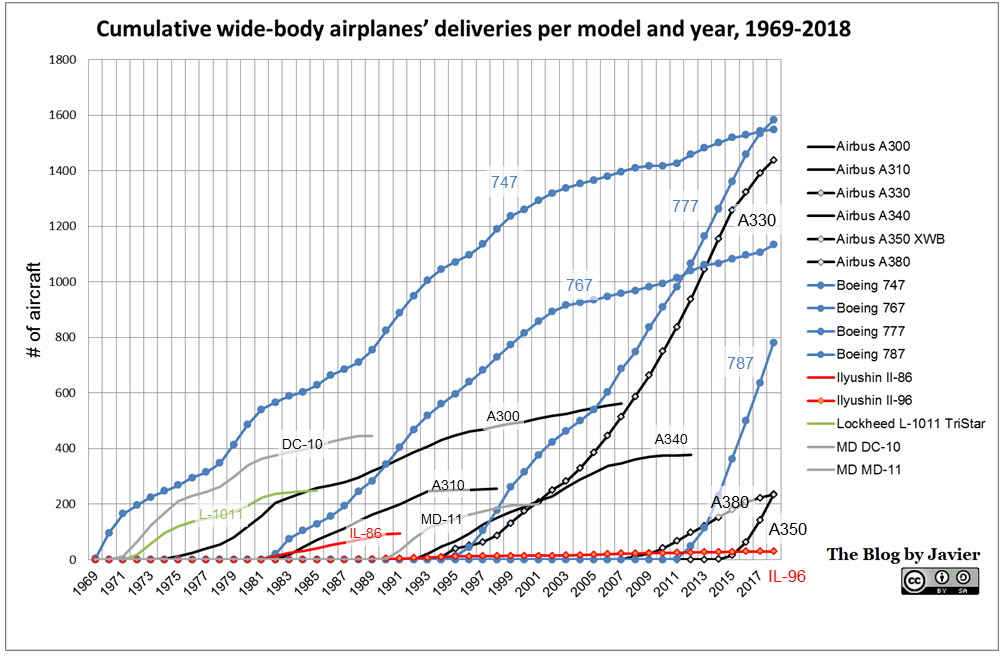

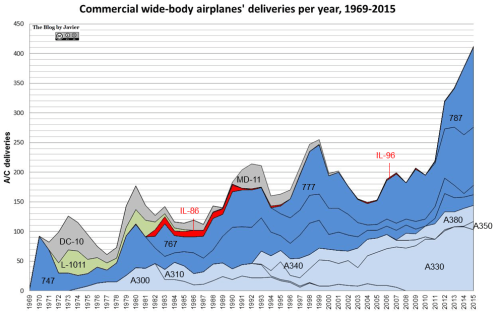

The first wide body commercial airplane, the first twin-aisle ever, the Boeing 747 first flew in February 9th 1969 and it was first delivered to a customer (Pan Am) in December 1969. In the following years new wide bodies arrived to the market: the Douglas DC-10 (in 1971), the Lockheed TriStar (1972), the Airbus A300 (1974)…

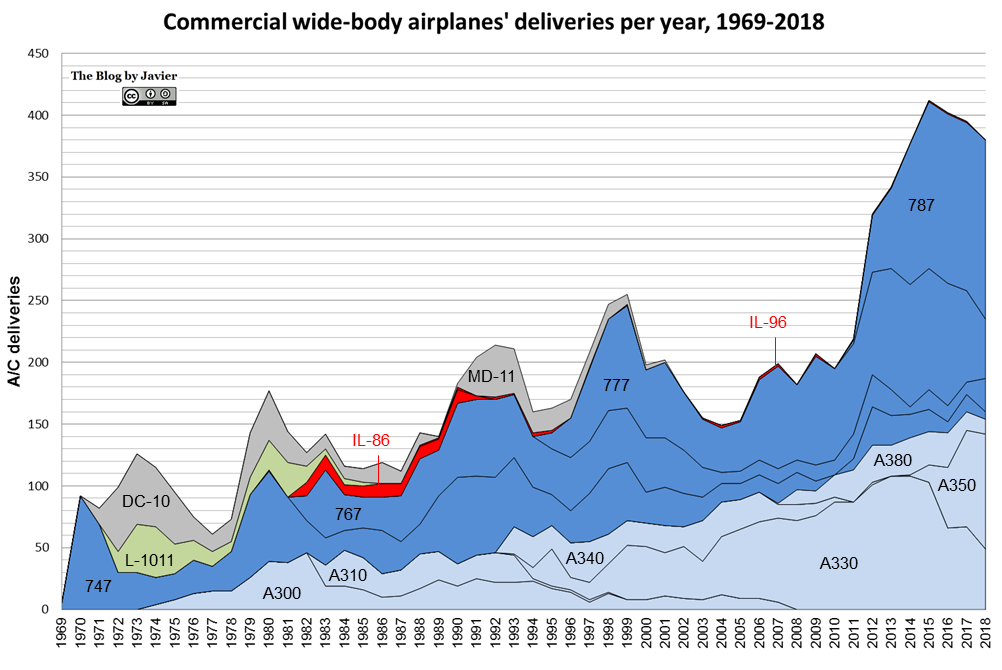

In the last weeks, both Airbus and Boeing have released the figures of aircraft deliveries for the complete 2015. With them I updated a graphic I had made back in 2013 with the commercial wide-body airplanes’ deliveries per year. Take a look at it.

Commercial wide-body airplanes’ deliveries per year, 1969-2015.

Some reflections:

For the first time ever, over 400 twin-aisle aircraft were delivered in a year. The feat is remarkable.

The average number of deliveries for the previous 20-year period (1995-2014) was 215 airplanes per year. Up to now, in the previous 46 years of twin-aisle market, in only 3 years more than 300 airplanes were delivered in a single year (the previous 3: 2012, 2013 and 2014) and only 12 times more than 200 airplanes had been delivered (including the previous 3 with more than 300).

The combined steep production ramp-up during last 4 years has enabled to reach a production rate of almost the double of what was produced just 5 years ago. In particular, the combined compound annual growth rate (CAGR) of the rate of deliveries for the last 5 years has been 16.1%, for the last 10 years 10.4%. These rates are the triple and double than the yearly growth of traffic (measured in RPKs).

With the figures up to the end of 2015, almost 8,000 wide-body airplanes had been delivered. Thus, by now, end of January 2016, we have certainly reached the figure (1). We however don’t know whether the 8,000th twin aisle was a Boeing or an Airbus (2).

The share of deliveries in 2015: 65% Boeing and 35% Airbus. Boeing has slightly increased its share of deliveries in the last 4-5 years, in particular with the ramp-up of the 787.

There were 135 787s delivered in 2015. That is another remarkable feat: the largest amount of twin-aisle deliveries of a single model in a single year ever.

Only 6 times ever (combination of model-year) have there been twin-aisle deliveries of over a hundred airplanes: the A330 in the last 4 years (with a peak of 108 airplanes in 2013 -then a record- and 2014) and the 787 the last two years. Only other 10 times there were deliveries of more than 80 airplanes of a single model in a year: the A330 (2010-2011), the 747 in 1970 and the 777 (7 times, including the last 4 years consecutively, out of which the last 3 on the verge of 100 deliveries – 98, 99, 98).

Two days ago Boeing released its 2015 earnings, and with it news of 777 production cut came up. Some time before similar news had come of 747 production rate decrease. With these news, quickly came comments of whether aerospace cycle may have peaked (see here). Looking backwards it’s clear that 2015 was a peak in wide-bodies deliveries. Looking forward it may have been a short-term peak, but looking further ahead it is not so clear. I will leave for another post the outlook of past deliveries mixed with what Airbus and Boeing market forecasts say (GMF and CMO, respectively).

—

(1) With the sources I used, at the end of 2015 there were a combined 7,988 wide-bodies delivered. However, I found different figures for the deliveries of the Ilyushin IL-86 (between 95 and 106). In any case, both figures would leave the total tally below 8,000 (making 2016 “the year of the 8,000th delivery”); I took for the analysis most conservative figure.

(2) Working at the moment for the Airbus A330neo programme, I will assume the 8,000th delivery was an A330, rather than a Boeing.

(3) I have indicated in the post that we have just passed the mark of 8,000 wide-bodies delivered since 1969, and, on the other hand, the different studies state that there are about 4,900 twin-aisle in operation. The gap of ~3,100 airplanes corresponds to those retired, parked, scrapped, crashed, displayed in museums…