Last week, on the first day of Farnborough air show, Airbus released the new figures of the 2016-35 Airbus’ Global Market Forecast (GMF, PDF 2.6 MB). This is good news, as it did so at the same time as Boeing released its Current Market Outlook (see a post here about it) and before it used to do so in September.

In previous years, I have published comparisons (1) of both Airbus’ and Boeing’s forecasts (Current Market Outlook, CMO, PDF 4.1 MB). You can find below the update of such comparison with the latest released figures from both companies.

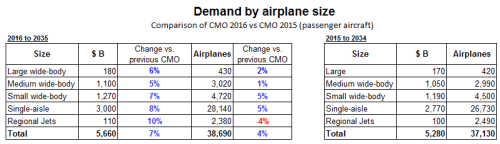

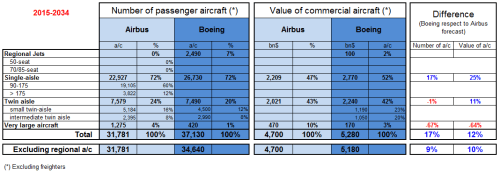

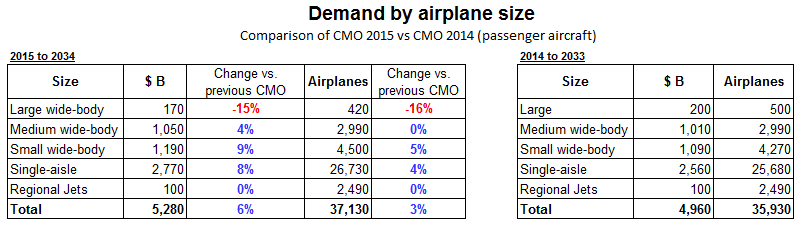

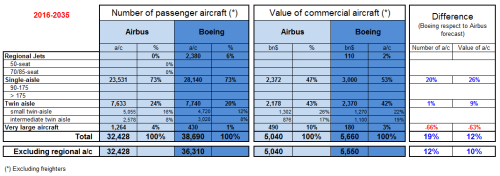

Comparison of Airbus GMF and Boeing CMO 2016-2035.

Some comments about the comparison:

- Boeing sees demand for 12% more passenger aircraft (excluding regional a/c) with a 10% more value (excluding freighters). The gap is higher than in 2015 (similar to 2013 and previous years).

- In relation to last year studies, Airbus has increased demand by ~650 aircraft whereas Boeing has increased by 1,670.

- Boeing continues to play down A380 niche potential (66% less a/c than Airbus’ GMF).

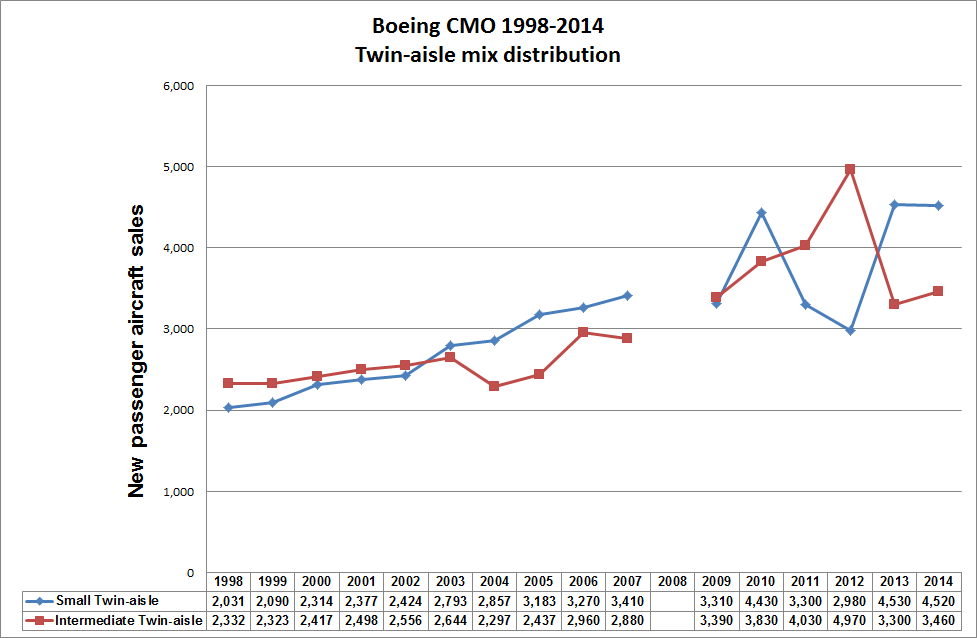

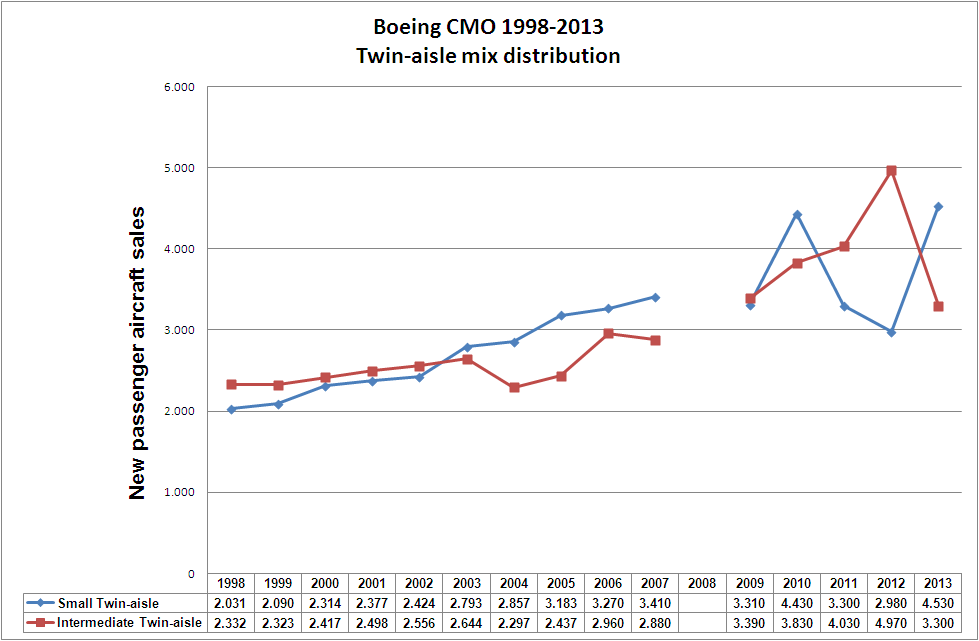

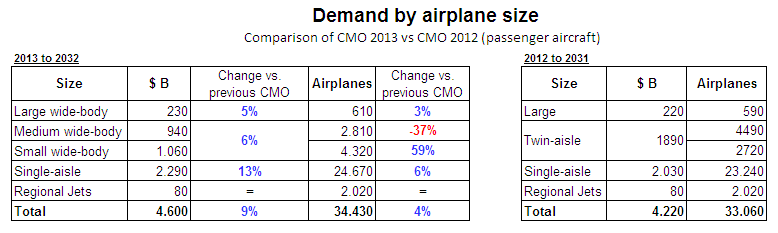

- Both companies’ forecast for the twin aisle segment is nearly identical: ~7,600-7,700 aircraft (Airbus sees demand for about a 100 less aircraft than Boeing, mainly due to Boeing increased figures in relation to 2015). The mix between small and intermediate twins varies, ~300-400 units up and down. However, Boeing’s wide-bodies mix is not to be taken as engraved in stone, see the erratic trend in the last years here.

- On the other hand, Boeing forecasts about 4,600 single-aisle more than Airbus (the gap has widened in 800 units this year). Boeing doesn’t provide the split between more or less than 175 pax capacity airplanes since its 2015 CMO, this year Airbus hasn’t included it either.

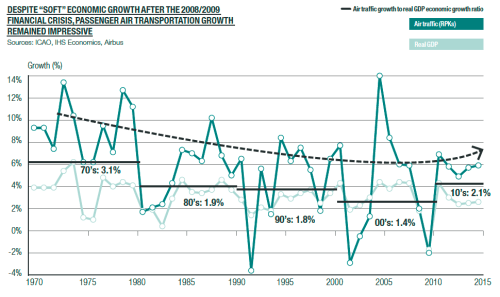

- In relation to traffic, measured in terms of RPKs (“revenue passenger kilometer”), that is, the number of paying passenger by the distance they are transported, they see a similar future: Airbus forecasts for 2035 ~16.0 RPKs (in trillion, 4.5% annual growth from today) while Boeing forecasts 17.01 RPKs (4.8% annual growth).

The main changes from last year’s forecasts are:

- Both manufacturers have increased their passenger aircraft forecast in between ~650-1,670 a/c.

- Both manufacturers have increased the volume (trn$) of the market in these 20 years, by about 300-400 bn$.

Some lines to retain from this type of forecasts:

- Passenger world traffic (RPK) will continue to grow about 4.5% per year (4.8% according to Boeing). This is, doubling every ~15 years.

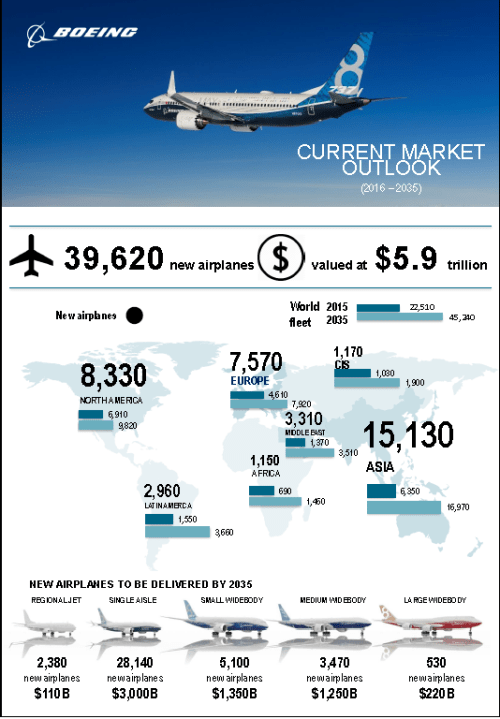

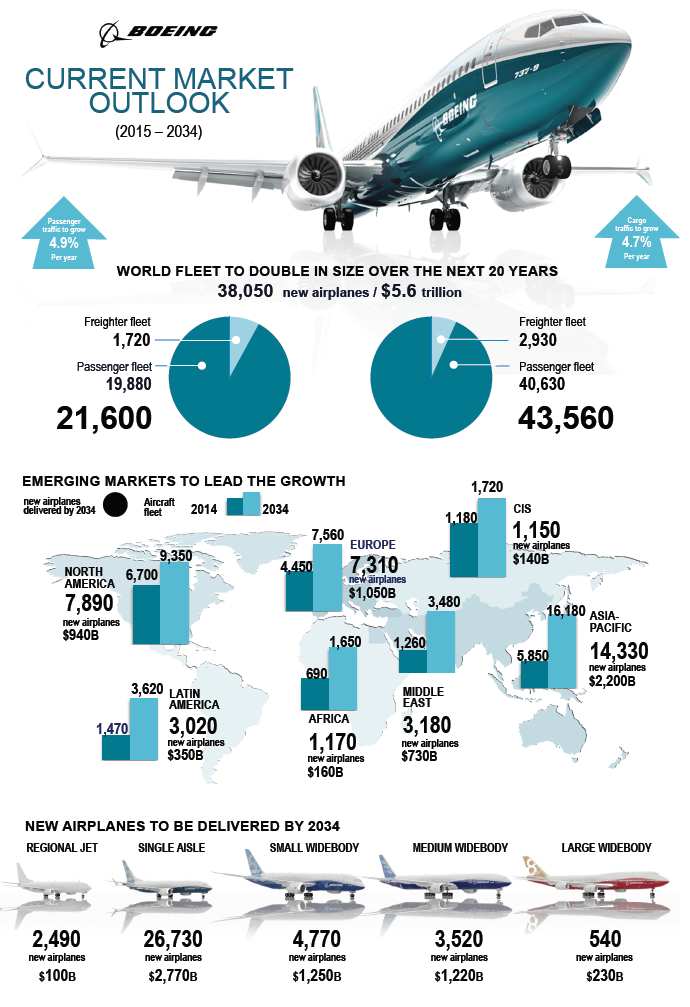

- Today there are about 18,019 passenger aircraft around the world (according to Airbus; 18,190 in Boeing’s CMO), this number is about 700 a/c more than the year before (4% increase) and will more than double over the next 20 years to 37,708 a/c in 2035 (39,750 as seen by Boeing, excluding regional jets).

- Most deliveries will go to Asia-Pacific, 41% or 13,239 passenger aircraft (according to Airbus).

- Domestic travel in China will be the largest traffic flow in 2035 with over 1,600 bn RPK (according to Airbus (x 3.7 times more than today’s traffic), or 1,897 bn RPK according to Boeing), or 11% of the World’s traffic.

- About 12,830 aircraft will be retired to be replaced by more eco-efficient types.

Passenger traffic growth vs. global GPD growth.

As I do every year, I strongly recommend both documents (GMF and CMO) which provide a wealth of information of market dynamics. This year, Airbus included as well an excel file with its data, find it here [XLS, 0.3 MB]

—

(1) Find here the posts with similar comparisons I made with the forecasts of previous years: 2015, 2014, 2013, 2012, 2011, 2010.