Next January 31st, Boeing will hold an earnings conference where it will announce its Q4 and full 2017 year financial results, including the revenues of each of its units.

Three weeks ago, on January 9th, Boeing already issued a press release where it announced its deliveries and orders for 2017, mainly:

- 763 commercial aircraft delivered (including 529 of the 737 family, or 136 787).

- 912 net orders (after cancellations) (including 745 of the 737 family).

The release mentions “912 net orders, valued at $134.8 billion at list prices“, however those list prices are discounted, nothing new, and with an estimate of that discount I’ll try to guess the figure of revenues for the Boeing Commercial Airplanes division, not so much trying to be accurate in itself, but to point in advance to the increasing of the discounts as we will see below.

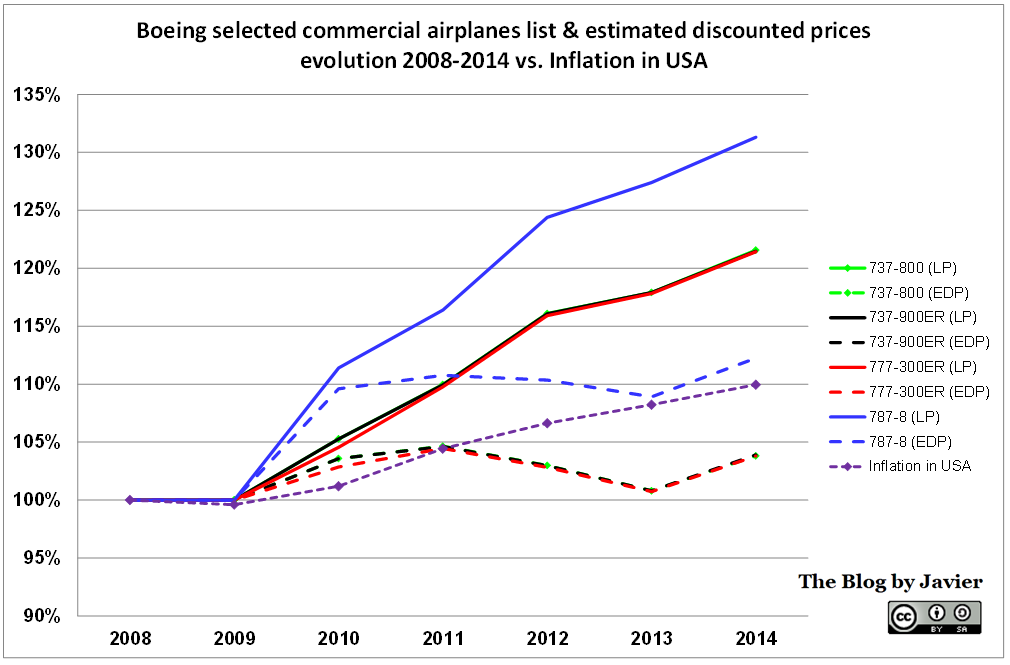

Where can we find Boeing list prices? Boeing host them in their site, these have just bee raised 10 days ago about 4% (see this comment about it). The previous prices dated from March 2017, when Boeing raised them again, that time by about 2% from its 2015 prices (untouched in 2016). To compute 2017 revenues and estimate of discount I use 2017 prices, not the latest ones.

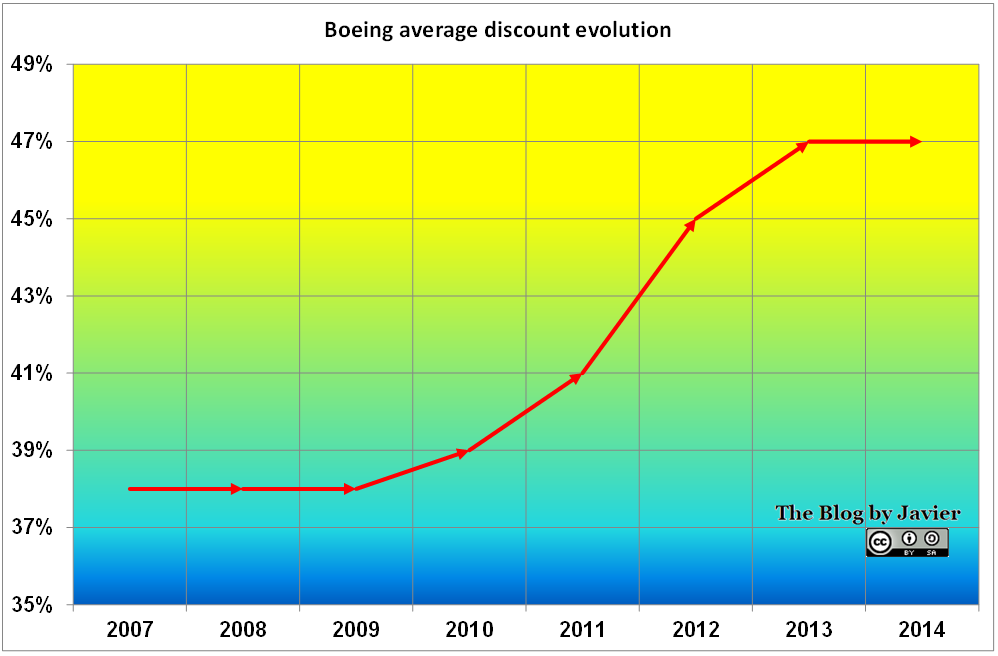

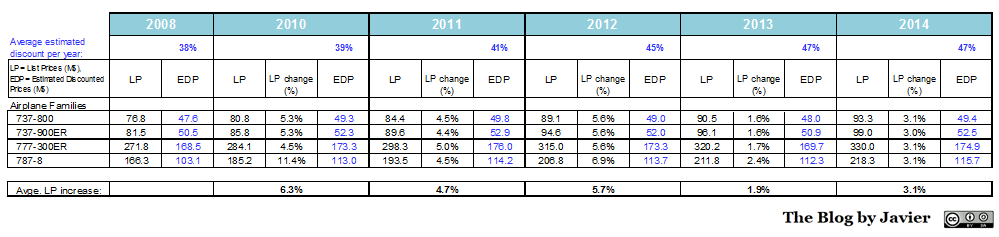

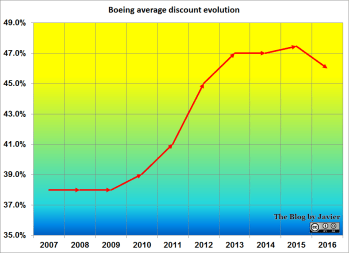

If Boeing didn’t apply those discounts, the value of the 763 aircraft delivered in 2017 would yield revenues of above 118 bn$. To come to a ballpark figure, I will take the latest figure of discounts that I had calculated with 2016 and earlier figures, being the latest ~46%.

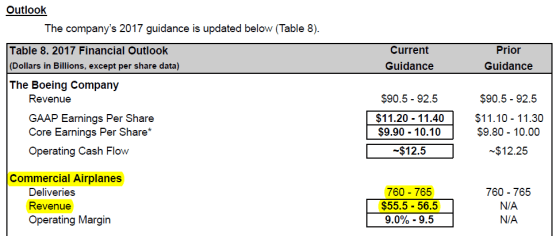

If I plug that discount into the 2017 list prices of the fleet mix of the 763 commercial aircraft that Boeing delivered we would come to a figure of revenues of 62.1 bn$. However, see below what was Boeing’s own guidance in their Q3 earnings release:

Boeing’s 2017 Financial Outlook at Q3 2017 earnings press release.

At three months to the year end (Q3), they forecast between 760 and 765 deliveries, which turned in 763. At the same time they pointed to revenues between 55.5 – 56.5 bn$… and not above 62 bn$. I believe they will exceed their own estimate, but not by 5 bn$, that is why I see that their discounts have been greatly increased in the last 2017. They must have had a bad time in escalating prices of aircraft sold years ago, delivered in 2017 but with escalation conditions much lower than ongoing list prices.

With all these ingredients… my forecast is: 57.0 bn$.

Some comments to it:

- My forecast is a bit more optimistic than their upper bracket (56.5) which may be slightly conservative.

- The implied discount of my revenues forecast would be in the ~ 50% range.

(1) See here a couple of such forecasting revenues exercises that I did for Boeing’s 2014 and 2015 revenues.

(2) See here the latest detailed calculation of discounts that I posted in 2015.