Recently, the 2016 UEFA Champions League final (between Real Madrid and Atletico de Madrid) was decided in a penalty shoot-out, so was the 2016 Copa America Centenario final (Chile – Argentina) and so have already been a couple of matches in the round of 16 and quarter finals of the ongoing UEFA Euro 2016 (Switzerland – Poland and yesterday’s Poland-Portugal). You could expect one or two more matches in that competition to be decided in such a way.

“The penalty shoot-outs are a lottery”

This is a mantra repeated once and again each time the extra time of a football match comes to an end and the score is still a draw. Yet penalty shoot-outs are not a lottery. However, asking TV or radio football commentators to describe this aspect of the game as “two-person zero-sum game that meets von Neumann’s Minimax theorem” would be too much.

Years ago, while reading the book “Soccernomics“, by Simon Kuper and Stefan Szymanski (book review here), I came to know a couple of papers on penalties and penalty shoot-outs published by the Spanish economist Ignacio Palacios Huerta (at the London School of Economics).

Penalties

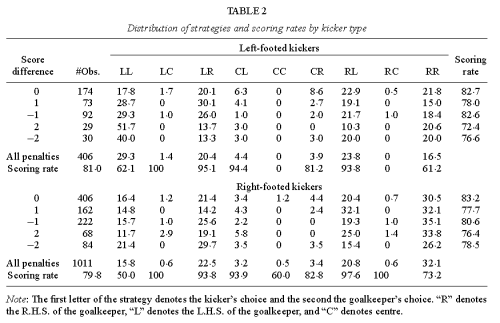

In a first paper, “Professionals Play Minimax“ (2002, and its annex) [PDF, 335 KB and 342 KB], by analyzing over 1,400 penalty kicks, he came to confirm that professionals do play Minimax, a game theory rule decision model in which they try to minimize the worst outcome not knowing the strategy of their opponent.

The object of the paper itself is to try to find a natural setting in which von Neumann’s theorem implication can be tested. Penalty kicks turns out to be such a natural setting, the reasons enabling the game to be so are: there are few strategies available to the players (basically shooting left or right for the kickers, or jumping to his left or right for the keepers), it is a two-player zero-sum game and the outcome of the game (goal or no goal) is immediate after a strategy is chosen.

Studying those over a thousand penalties and in particular those of 42 players (kickers and keepers) who have been each one involved in over 30 penalties in the time span of the study (1995-2000), the author came to the following findings:

- Kickers have practically the same probability of scoring with different mix of strategies (being a strategy alternating between shooting left or right by a given proportion).

- Players are capable of generating truly random sequences of choices (left – right). This is remarkable, as humans, when asked to produce a random sequence, normally over do it and shy away from what would be truly random.

- Some figures: players shoot to their natural side (with the interior of the feet, shooting left to a right footed) just above 50% of the times, keepers jump to the natural side of the kicker slightly more often.

- When the keeper “guesses” the side to which the kicker is shooting, the scoring probability greatly differs depending on whether it was the kicker’s “natural side”, 71%, or the non-natural side, 55%. When the keeper jumps to the wrong side the scoring probability is about 95% with no big difference between natural or non-natural side.

- During a match the average scoring rate is about 80%, with the rate decreasing as the match comes to an end (73% for penalties in the last 10 minutes).

- Some players during the years of the study (1995-2000) had significantly better scores; in particular Mendieta (91% and no matter whether he kicked to his natural (68% of the times) or non-natural side (32%)), Del Piero and Juninho (especially strong on their natural side (94%) and above average in their non-natural (87%)) or Bergkamp (91% and 88%).

- Strategies between players varied greatly. As I said Mendieta had a 68/32 (natural / non-natural), whereas Batistuta had a 81/19 and Baggio a 45/55, all with above average scoring success. Other players like Zidane, Mihajlovic or Chiesa managed an undistinguishable 50/50.

See a couple of interesting tables below:

Even more interesting is his second paper.

Penalty shoot-outs

In a second paper, “Psychological Pressure in Competitive Environments: Evidence from a Randomized Natural Experiment” (2009, with Jose Apesteguia) [PDF, 342 KB], Palacios Huerta wants to find out how emotions play a major effect on performance and to do so he takes a look at penalty shoot-outs from major football competitions.

For this study he reviewed over 2,800 penalty kicks in about 270 penalty shoot-outs. He divides the observations in two blocks, before and after FIFA changed the rules governing the shoot-outs in 2003. Before that date, the team of the captain winner of a toss of a coin started kicking first; after the change in the rules, the captain winner of the toss of a coin chooses which team kicks first.

Before 2003, the fact of kicking first or not was random, and after 1,343 kicks in 129 shoot-outs, the authors found out that the first in kicking in the sequence win the penalty shoot-out 60.5 percent of the time. (1)

As part of his study, Palacios Huerta made a survey questioning over 200 football players and coaches in Spain, professionals and amateurs, what would they choose if they had won the toss of a coin to decide which team kicks first in a penalty shoot-out. The results offer not doubt: over 95% of the cases chose to kick first. When asked why they would choose that option they indicated “to put pressure on the rivals”.

Experience matched the survey. After the change of FIFA rules in 2003, Palacios Huerta gathered data of another 140 penalty shoot-outs up to 2008 (just before writing his paper). Those were the first 140 penalty shoot-outs in which the winner of the toss of a coin had to choose whether he wanted his team to kick first or his opponent to kick first. In just a single case did the winner of the toss of a coin choose to let the opponent to kick first: Gianluigi Buffon playing for Italy the quarter-final of the Euro cup in 2008 against Spain, with the result that Spain won the penalty shoot-out and went to win the Euro, starting a streak of 3 consecutive major competitions at national level (Euro 2008, World Cup 2010 and Euro 2012).

Take a look at the following graphics and tables that let you read how the probabilities of scoring each penalty in a shoot-out evolve depending on previous outcomes (whether the team is behind, even or ahead) and the probability of winning the shoot-out (hence qualifying to the next phase or winning the competition) evolve.

I highlighted in the previous table in blue and yellow the scoring probability for each kick and the winning percent of the shoot-out for a shoot-out in which both teams go about scoring each of the penalties. It is interesting, if not dramatic, to see how while the scoring probability for the first team is always between 72 and 78% (2), for the second team it drops from 82% to 62-66% for rounds 3 to 5. Similarly, the winning probability decreases for the second team down to 21-23% just before attempting kicks 3 and 4 if all previous penalties have been scored.

See below that 2008 penalty shoot-out between Spain and Italy.

—

After having commented on these two papers and its conclusions, let me share a few comments and anecdotes:

MILAN, ITALY – MAY 28: Cristiano Ronaldo of Real Madrid scores the winning penalty during the UEFA Champions League Final. (Photo by Shaun Botterill/Getty Images)

Toss of a coin. Both 2016 Copa America Centenario final and UEFA Champions League final were won by the team which kicked the first penalty, Chile and Real Madrid, respectively. In the draw, using the toss of a coin, to decide which team kicked first Chile chose to kick first (see here the video). However, in the Champions League final, Atletico de Madrid’s captain Gabi chose to let Real Madrid kick first. Apparently, he chose that as they had kicked second in the round of 16 of that same competition against PSV Eindhoven and passed. Somehow he tried to repeat the sequence thinking that this would bring them luck. Well, with that decision he put his team against about 60-40% odds backed by over 30 years of recorded experience and about 270 shootouts. Not a clever move. See this article “La buena mala suerte del Churu” by Manuel Jabois discussing this toss of a coin (in Spanish). See here the video.

“[…] we find a systematic first-mover advantage. Further, professionals are self-aware of their own psychological effects and, when given the chance, they rationally react by systematically taking advantage of these effects.” (Palacios-Huerta)

As reflected above, in the paper, Palacios-Huerta indicates that between 2003 and 2008 only once in 140 samples did the winner of the toss chose to let the opponent kick first. That is why it was striking what Gabi did and why it called the attention of some football fans. Well, yesterday, during the first match of the Euro 2016 quarter finals between Poland and Portugal, we had yet another such example, another anomaly. This time it was Robert Lewandowski, the Polish captain, the perpetrator. He won the toss of the coin and chose that Portugal kicked first. I can imagine how Cristiano Ronaldo might have felt at that moment, the second time in just 6 weeks that he was being handed such a present. Portugal won the shoot-out.

As reflected above, in the paper, Palacios-Huerta indicates that between 2003 and 2008 only once in 140 samples did the winner of the toss chose to let the opponent kick first. That is why it was striking what Gabi did and why it called the attention of some football fans. Well, yesterday, during the first match of the Euro 2016 quarter finals between Poland and Portugal, we had yet another such example, another anomaly. This time it was Robert Lewandowski, the Polish captain, the perpetrator. He won the toss of the coin and chose that Portugal kicked first. I can imagine how Cristiano Ronaldo might have felt at that moment, the second time in just 6 weeks that he was being handed such a present. Portugal won the shoot-out.

Palacios Huerta and other analysts receive requests for dedicated reports about kicking patterns, records and data of different teams when playing knock-out phases. In Soccernomics, Simon Kuper and Stefan Szymanski, describe how that happened during the 2008 UEFA Champions League final between Manchester United and Chelsea. Palacios Huerta had given Chelsea some tips on Manchester kickers and keeper (van der Saar): “Van der Sar tends to dive to the kicker’s natural side”, “most of the penalties that Van der Sar stops are mid-height, thus is better to shoot low or high”, “if Cristiano Ronaldo stops half-way in the run-up to the ball chances are 85% that he shoots to his natural side”…, it is quite interesting to actually see that penalty shoot-out and how the different players acted. See below the video. Apparently Van der Saar saw how Cech, Chelsea’s keeper had some paper in his hands and also noticed how kickers were shooting to their non-natural side, until at the 7th penalty (~9’30” in the video) he defies Anelka by pointing to Anelka’s non-natural side, like saying “I know you have the tip to kick there”, then…

For the record, the final was won by Manchester, first in kicking.

Finally, ever since coming to know all this information I have enjoyed penalty shootouts more than before. I now entertain myself seeing the strategy taken by the keepers and kickers, whether the keeper jumps to the natural side of the kicker more or less than in 60% of the shots, if he changes his strategy depending on whether the kicker is left or right-footed, whether kickers shoot more or less than 60% of the shots to their natural side, etc.

“Les grandes personnes aiment les chiffres“, Le Petit Prince.

—

(1) At the time of the Copa de America Centenario final, the Spanish journalist Alexis Sanchez (better know by his profile @2010MisterChip), expert in providing all kind of football statistics, tweeted that Chile, being the first in kicking in the penalty shootout against Argentina had a 55% chance of winning the tournament. Thus, it may be the case that he has a larger (not public) database including more penalty shootout.

(2) Note how probabilities in shoot-outs decrease from the average of 80% of penalties during the match.